a)

To calculate: The following:

- Short-run supply curve for each snuffbox maker

- Short-run supply curve for the market as a whole

a)

Answer to Problem 9.8P

- Short-run supply curve for each snuffbox maker is

- Short-run supply curve for the market as a whole is

Explanation of Solution

Given:

Total identical firms

Short-run total cost

Short-run marginal cost

Explain:

- In the

perfect competition , supply curve for each firm will be equal to its short-run marginal cost. - As there are 100 firms in the industry thus industry supply is given as follows:

Thus, the short-run supply curve for each snuffbox market is

Introduction: One of the portion in the marginal cost that will appear above its

b)

To Calculate: The following:

- Equilibrium in the market

- Each firm’s total short-run profit

b)

Answer to Problem 9.8P

- Equilibrium in the market is

- Each firm’s total short-run profit is

Explanation of Solution

Given:

Explain:

a)

For equilibrium

Calculate the equilibrium as follows:

Set

b)

Calculate the equilibrium quantity as follows:

Substitute the value of P in the equation to get the value of Q.

Thus, the equilibrium quantity is

As there are 100 firms, each firm will produce

The formula for calculating total profit as follows:

Calculate TC as follows:

Thus, the firms total cost is

Calculate the firm’s total revenue as follows:

Thus, the total revenue is

Calculate the total profit as follows:

Thus, the firms total short run profit is

Introduction: Equilibrium is one of the market price where supplied goods is similar to the demanded goods. In this place only demand and supply curves in the market intersect. During

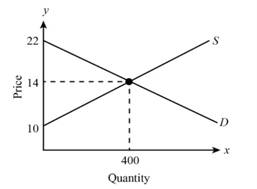

c)

To Graph: The market equilibrium and compute total

c)

Answer to Problem 9.8P

Total producer surplus is

Explanation of Solution

In the graph, quantity is represented on the horizontal axis and price on the vertical axis.

Equilibrium is at the point where demand and supply curve intersect each other.

Thus, the

Calculate the

Consumer surplus

Thus, the consumer surplus is

Calculate the producer surplus as follows:

Producer surplus

Thus, the Producer surplus is

Calculate the total surplus as follows:

Total surplus=Consumer surplus +Producer surplus

Thus, the total surplus is

Introduction: There is a great demand and equal supply, the markets are at equilibrium during summer. During post summer season, the supply will start falling and demand will remain the same. The corresponding price is the equilibrium price, also the quantity is the

d)

To Show: The calculated total producer surplus in part c is equal to total industry profits plus industry short-run fixed costs.

d)

Answer to Problem 9.8P

Total producer surplus is

Total industry profits and industry short-run fixed costs is

Therefore, the total industry profits plus industry short-run fixed cost is equal to producer’s surplus.

Explanation of Solution

Calculate the total profits of the industry as follows:

Total profit of the industry

Thus, the total profit of the industry is

Calculate the short run fixed costs as follows:

Thus, the short run fixed cost is

Because as per the equation,

Sum up both the total profit and short run fixed cost as follows:

Total profits+SRFC

Thus, it equals to

The producer surplus is

Introduction: Fixed costs are the expenditures that does not change based on the levels of production at least not in the short term. The fixed costs are same when the product will be produced a lot or little.

e)

To calculate: The tax change the market equilibrium when the government imposed a $3 tax on snuffboxes.

e)

Answer to Problem 9.8P

The market equilibrium price has declined from $14 to $13 and also the equilibrium quantity has declined by $100(from 400 to 300 units)

Explanation of Solution

Because of tariffs, new demand curve will be

Calculate the new equilibrium price as follows:

Thus, the equilibrium price is

Calculate the equilibrium quantity as follows:

Thus, the equilibrium quantity is

Introduction: Demanded quantity will be similar to the supplied quantity in a particular price is defined as Equilibrium. Suppose if the tax will be imposed by the government into the market, the tax imposed is to impact of the equilibrium. If the tax increases the price a buyer pays less than the tax.

f)

To Describe: The burden of the tax to be shared between snuffbox buyers and sellers.

f)

Answer to Problem 9.8P

Tax paid is

Consumers and producers will pay

Explanation of Solution

Calculate the tax paid as follows:

Tax paid

Introduction: Tax burden is divided between buyers and sellers. Suppose if the supply is more elastic than demand, buyers bear most of the tax burden. Otherwise, if the demand is more elastic than supply, producers bear most of the tax burden.

g)

To Calculate: The total loss of producer surplus as a result of the taxation of snuffboxes.

g)

Answer to Problem 9.8P

The total loss of producer surplus as a result of the taxation of snuffboxes are

Explanation of Solution

Calculate the producer surplus as follows:

Produce surplus

Thus, the producer surplus is

Calculate the total loss of producer’s surplus as a result of the taxation of snuffboxes as follows:

Total loss

Introduction: The difference between prices is that Producers are willing to sell a product based on their costs within price and market equilibrium price is defined as produce surplus. Suppose if the economy produces the inefficient quantity, total surplus will occur. Deadweight is loss in the total producer.

Want to see more full solutions like this?

Chapter 9 Solutions

EBK INTERMEDIATE MICROECONOMICS AND ITS

- Suppose the quantity of apples supplied in yourmarket is 2,400. If there are 60 apple producers,each with identical cost structures, how manyapples does each producer supply to the market?arrow_forwardSuppose that each firm in a competitive industry has the following costs: Totalcost:TC=50+1/2q2 Marginalcost:MC=q where q is an individual firm's quantity produced. The market demand curve for this product is Demand:QD=120−P where P is the price and Q is the total quantity of the good. Currently, there are 9 firms in the market.a. What is each firm's fixed cost? What is its variable cost? Give the equation for average total cost.b. Graph average-total-cost curve and the marginal-cost curve for qfrom 5 to 15. Atwhat quantity is average-total-cost curve at its minimum? What is marginal cost and averagetotal cost at that quantity?c. Give the equation for each firm's supply curve.d. Give the equation for the market supply curve for the short run in which the number of firms is fixed.e. What is the equilibrium price and quantity for this market in the short run?f. In this equilibrium, how much does each firm produce? Calculate each firm's profit or loss. Is there incentive for firms to…arrow_forwardThe figure depicts the demand curve of a firm producing cars, together with its marginal cost, average cost, and isoprofit curves. Based on this figure, which of the following statements are correct? 8,000 Price, Marginal cost ($) 0 E Quantity of cars, Q At A, the firm makes positive profits. The firm makes the same profit at B and D. O Profit margin is the same at B and D. O The slope of the isoprofit is zero at D. MC Isoprofit A Isoprofit B AC 100arrow_forward

- Firms in the market for soccer balls are selling in a purely competitive market. A firm in the soccer ball market has an output of 5,000 balls, which it sells for $10 each. At the output level of 5,000 the average variable cost is $6.00, the average total cost is $7.50, and the marginal cost is $10.00. What would you expect the firm to do in the short run? Why? What would you expect the market to do in the long run? Why?arrow_forwardSuppose the market for peaches is perfectly competitive. The short-run average total cost and marginal cost of growing peaches for an individual grower are illustrated in the figure to the right. Assume that the market price for peaches is $30.00 per box. What is the profit-maximizing quantity for peach growers to produce? boxes. (Enter your response as an integer.) At this level of output, profit will be $. (Enter your response rounded to the nearest dollar.) Peach growers will earn positive economic profit in the short run at any market price above $ per box. (Enter your response rounded to one decimal place.) Price (dollars per box) 40- 36- 32- 28- 24 20 16- 12- 8 4- 10 MC 20 30 40 50 60 70 80 Output (boxes of peaches per day) ▬▬ ATC 90 100 Qarrow_forwardSuppose that each firm in a competitive industry has the following costs: Total cost: TC = 50 + 1/2q2 Marginal cost: MC = q Where q is an individual firm’s quantity produced. The market demand curve for the product is: Demand: QD = 120 – P Where P is the price and Q is the total quantity of the good. Currently there are 9 firms in the market. What is each firm’s fixed cost? What is its variable cost? Give the equation for average total cost. Graph the average-total-cost curve and the marginal-cost curve for q from 5 to 15. At what quantity is the average-total-cost curve at its minimum? What is the marginal cost and average total cost at that quantity? Give the equation for each firm’s supply curve. Give the equation for the market supply curve for the short run in which the number of firms is fixed. What is the equilibrium price and quantity for the market in the short run? In this equilibrium, how much does each firm produce? Calculate the firm’s profit and loss. Do firms have…arrow_forward

- Suppose the market for peaches is perfectly competitive. The short-run average total cost and marginal cost of growing peaches for an individual grower are illustrated in the figure to the right. Assume that the market price for peaches is $28.00 per box. What is the profit-maximizing quantity for peach growers to produce? boxes. (Enter your response as an integer.) Price (dollars per box) 40- 36- 32- 28- 24- 20- 16- 12- 8- 4- 0 10 20 30 40 50 60 70 80 Output (boxes of peaches per day) MC ATC 90 100 oo Qarrow_forwardThe diagram shows a price-taking bakery's marginal and average cost curves, and its isoprofit curves. The current market price for bread is P*= 2.50. Which of the following statements is correct? 8 Price, P (€); cost 4 3.70 2.50 2 0 0 Select one: 20 40 60 80 100 120 140 Quantity of loaves, Q 160 180 O a. The bakery is a price setter and sets its price as 2.50. b. The bakery maximises its profits by supplying 160 loaves. O c. The bakery's profit is 200. Marginal cost curve Isoprofit curve: €200 Isoprofit curve: €80 Firm's demand curve Zero-economic- profit curve (AC curve) 200 O d. The bakery's profit decreases until the quantity is 120, and then increases. e. The marginal cost curve is the bakery's supply curve.arrow_forwardThe following table displays the average cost of producing a good at different levels of output in the long run. Output (units) Average Cost ($) 940 190 980 140 1,020 120 1,060 110 1,100 110 1,140 125 1,180 145 if all the firms in the market have the same LRAC curve, what is the minimum level of output needed for a low-cost firm to compete in the market? Write the exact answer. Do not round.arrow_forward

- Assume that a firm in a competitive market faces the following cost information. If the market price for this firm's product is $40, calculate the profit maximizing level of output for this firm using marginal analysis. It may help to create your own cost table and fill in columns for Marginal Cost and Average Total Cost based on the Total Cost information below. a.What is the level of profit for this firm at the profit maximizing output? b.To convince yourself that the quantity you found is indeed the profit maximizing quantity, try calculating what the profit would be at the next higher level of output. What did you find? c. What do you predict will happen in this market over the long run?arrow_forwardEach of 1,000 identical firms in the competitive peanut butter industry has a short-run marginal cost curve given by SMC = 3 + Q. If the demand curve for this industry is P= 12 1,000 ? what will be the short-run loss in producer and consumer surplus if an outbreak of aflatoxin suddenly makes it impossible to produce any peanut butter? Instructions: Round your answers to the nearest whole number. Producer surplus: $ Consumer surplus: $arrow_forwardSuppose there are 100 identical firms in the perfectly competitive notecard industry. Each firm has a short- 9.3. run total cost curve of the form: 1 STC =9 + 0.2q² + 4q + 10 300 and marginal cost is given by SMC = .01q² + .4q+ 4 a. Calculate the firm's short-run supply curve with q (the number of crates of notecards) as a function of market price (P). b. Calculate the industry supply curve for the 100 firms in this industry. c. Suppose Q = -200P + 8,000. What will be the shortrun equilibrium price-quantity combination? d. Suppose everyone starts writing more research papers and the new market demand is given by Q = -200P + 11,200. What is the new short-run price-quantity equilibrium? How much profit does each firm make? market demand is given byarrow_forward

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning