Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN: 9781337788281

Author: James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 8, Problem 7RE

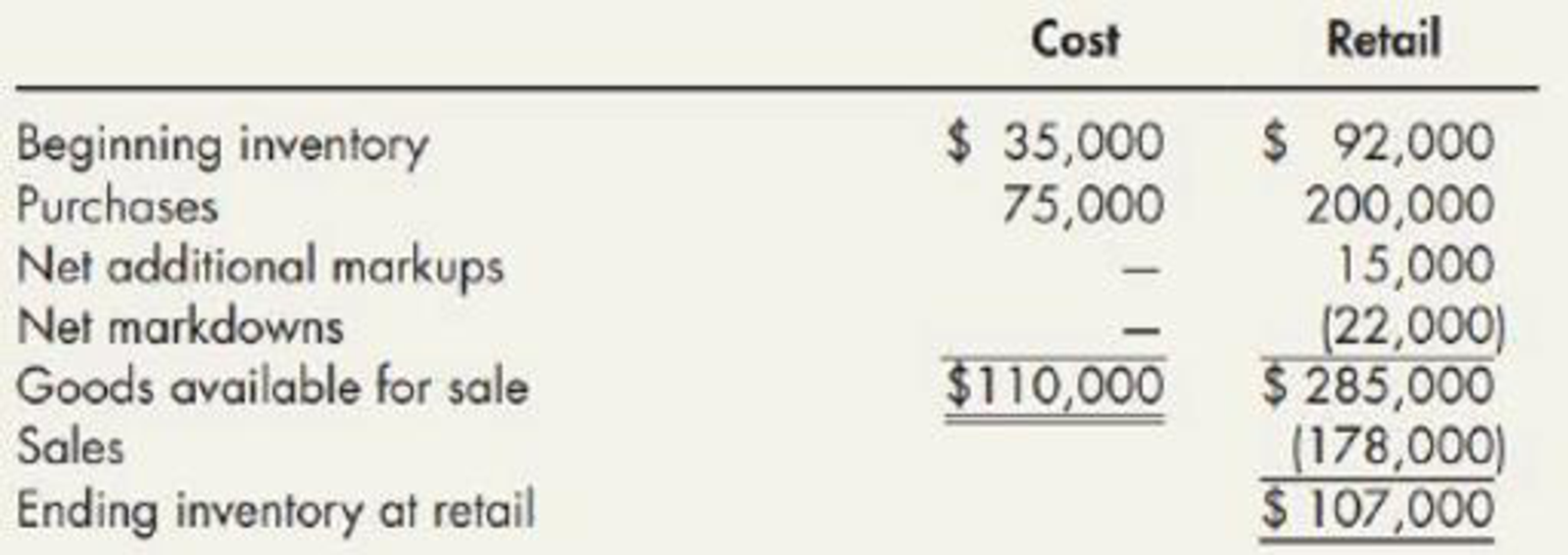

Uncle Butch’s Hunting Supply Shop reports the following information related to inventory:

Calculate Uncle Butch’s’ ending inventory using the retail inventory method under the FIFO cost flow assumption. Round the cost-to-retail ratio to 3 decimal places.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

MusicMagic specializes in sound equipment. Company records indicate the following data for a line of speakers:

(Click the icon to view the data.)

Read the requirements.

Co

Requirement 1. Determine the amounts that MusicMagic should report for cost of goods sold and ending inventory two ways: a. FIFO and b. LIFO. (MusicMagic uses a perpetual inventory

system.)

Start by determining the amounts that MusicMagic should report for cost of goods sold and ending inventory under a. FIFO.

FIFO method cost of goods sold =

FIFO method ending inventory =

Data table

Date

Mar 1

Mar 2

Mar 7

Mar 13

Item

Balance

Purchase

Sale

Sale

Print

Quantity

14

5

7

6

Unit Cost

$

Done

41

48

Sale Price

$

109

102

X

Salmone Company reported the following purchases and sales of its only product. Salmone uses a periodic inventory system. Determine the cost assigned to ending inventory using LIFO.

Assume that Whitewall Tire Store completed the following perpetual inventory transactions for a line of tires:

i (Click the icon to view the transactions.)

Read the requirements.

Requirement 1. Compute cost of goods sold and gross profit using the FIFO inventory costing method.

Begin by computing the cost of goods sold and cost of ending merchandise inventory using the FIFO inventory costing method. Enter the transactions in chronological order, calculating new inventory on hand balances after each transaction. Once all of the transactions have

been entered into the perpetual record, calculate the quantity and total cost of merchandise inventory purchased, sold, and on hand at the end of the period. (Enter the oldest inventory layers first.)

Date Quantity

Dec. 1

11

23

261

29

Totals

Purchases

Unit

Cost

Cost of Goods Sold

Total

Unit

Cost Quantity Cost

Total

Cost

Inventory on Hand

Unit

Quantity Cost

C

Total

Cost

More info

Dec. 1 Beginning merchandise inventory

Dec. 11 Purchase

Dec. 23…

Chapter 8 Solutions

Intermediate Accounting: Reporting And Analysis

Ch. 8 - Under what circumstances will a company value...Ch. 8 - What is the conceptual justification for reducing...Ch. 8 - Define the terms cost, net realizable value, and...Ch. 8 - For companies that use either LIFO or the retail...Ch. 8 - What three implementation approaches may a company...Ch. 8 - Describe the two approaches to recording the...Ch. 8 - Prob. 7GICh. 8 - In applying the inventory valuation rules to...Ch. 8 - Prob. 9GICh. 8 - What are the exceptions to historical cost...

Ch. 8 - Prob. 11GICh. 8 - Prob. 12GICh. 8 - What is the basic assumption underlying the gross...Ch. 8 - Prob. 14GICh. 8 - Prob. 15GICh. 8 - Explain the meaning of the following terms:...Ch. 8 - Prob. 17GICh. 8 - Prob. 18GICh. 8 - The retail inventory method indicated an inventory...Ch. 8 - Prob. 20GICh. 8 - Indicate the effect of each of the following...Ch. 8 - Sienna Company uses the FIFO cost flow assumption....Ch. 8 - Moore Company uses the LIFO cost flow assumption...Ch. 8 - A company uses the LIFO cost flow assumption. The...Ch. 8 - Prob. 4MCCh. 8 - Hestor Companys records indicate the following...Ch. 8 - Under the retail inventory method, freight-in...Ch. 8 - The retail inventory method would include which of...Ch. 8 - At December 31, 2019, the following information...Ch. 8 - Estimates of price-level changes for specific...Ch. 8 - A company forgets to record a purchase on credit...Ch. 8 - Brown Company has the following information...Ch. 8 - Black Corporation uses the LIFO cost flow...Ch. 8 - Blue Corporation uses the FIFO cost flow...Ch. 8 - Paul Corporation uses FIFO and reports the...Ch. 8 - Using the information provided in RE8-4, prepare...Ch. 8 - Kays Beauty Supply uses the gross profit method to...Ch. 8 - Uncle Butchs Hunting Supply Shop reports the...Ch. 8 - Use the information in RE8-7. Calculate Uncle...Ch. 8 - Use the information in RE8-7. Calculate Uncle...Ch. 8 - Use the information in RE8-7. Calculate Uncle...Ch. 8 - Johnson Corporation had beginning inventory of...Ch. 8 - Borys Companys periodic inventory at December 31,...Ch. 8 - Refer to the information provided in RE8-4. If...Ch. 8 - Refer to the information provided in RE8-4. If...Ch. 8 - Inventory Write-Down Stiles Corporation uses the...Ch. 8 - Inventory Write-Down Stiles Corporation uses the...Ch. 8 - Inventory Write-Down Byron Company has five...Ch. 8 - Inventory Write-Down The following information for...Ch. 8 - Inventory Write-Down The following information is...Ch. 8 - Inventory Write-Down The inventories of Berry...Ch. 8 - Prob. 7ECh. 8 - Gross Profit Method: Estimation of Flood Loss On...Ch. 8 - Prob. 9ECh. 8 - Gross Profit Method: Estimation of Theft Loss You...Ch. 8 - Retail Inventory Method Harmes Company is a...Ch. 8 - Retail Inventory Method The following data were...Ch. 8 - Retail Inventory Method The following information...Ch. 8 - Dollar-Value LIFO Retail Johns Company adopts the...Ch. 8 - Dollar-Value LIFO Retail Wyatt Company adopts the...Ch. 8 - Dollar-Value LIFO Retail On December 31, 2018,...Ch. 8 - Errors A company that uses the periodic inventory...Ch. 8 - Errors During the course of your examination of...Ch. 8 - (Appendix 8.1) Inventory Write-Down The...Ch. 8 - Inventory Write-Down Palmquist Company has five...Ch. 8 - Inventory Write-Down The following are the...Ch. 8 - Inventory Write-Down The inventory records of...Ch. 8 - Gross Profit Method: Estimation of Fire Loss On...Ch. 8 - Gross Profit Method: Estimation of Flood Loss On...Ch. 8 - Retail Inventory Method Turner Corporation uses...Ch. 8 - Retail Inventory Method EKC Company uses the...Ch. 8 - Retail Inventory Method Red Department Store uses...Ch. 8 - Retail Inventory Method Weber Corporation uses the...Ch. 8 - Dollar-Value LIFO Retail The following information...Ch. 8 - Dollar-Value LIFO Retail Intella Inc. adopted the...Ch. 8 - Prob. 12PCh. 8 - Errors As controller of Lerner Company, which uses...Ch. 8 - Comprehensive: Inventory Adjustments Layne...Ch. 8 - (Appendix 8.1) Inventory Write-Down The following...Ch. 8 - (Appendix 8.1) Inventory Write-Down Frost Companys...Ch. 8 - Prob. 1CCh. 8 - Sandberg Paint Company, your client, manufactures...Ch. 8 - Prob. 3CCh. 8 - Inventory Valuation Issues Hanlon Company...Ch. 8 - Gross Profit Shelly Corporation is an importer and...Ch. 8 - Prob. 6CCh. 8 - Prob. 7CCh. 8 - Various Inventory Issues Hudson Company, which is...Ch. 8 - Analyzing Starbucks Inventory Disclosures Obtain...Ch. 8 - Analyzing Moet Hennessy Louis Vuittons (LVMH)...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Inventory Costing: Average Cost Refer to the information for Filimonov Inc. and assume that the company uses a perpetual inventory system. Required: Calculate the cost of goods sold and the cost of ending inventory using the average cost method. ( Note: Use four decimal places for per-unit calculations and round all other numbers to the nearest dollar.)arrow_forwardUse the last-in, first-out (LIFO) cost allocation method, with perpetual inventory updating, to calculate (a) sales revenue, (b) cost of goods sold, and c) gross margin for A75 Company, considering the following transactions.arrow_forwardBeginning inventory, purchases, and sales data for portable game players are as follows: The business maintains a perpetual inventory system, costing by the first-in, first-out method. a. Determine the cost of the merchandise sold for each sale and the inventory balance after each sale, presenting the data in the form illustrated in Exhibit 3. b. Based upon the preceding data, would you expect the inventory to be higher or lower using the last-in, first-out method?arrow_forward

- Use the first-in, first-out (FIFO) cost allocation method, with perpetual inventory updating, to calculate (a) sales revenue, (b) cost of goods sold, and c) gross margin for A75 Company, considering the following transactions.arrow_forwardUse the following information to compute cost of goods sold under the FIFO and LIFO inventory methods. The firm sold 200 units.arrow_forwardUse the last-in, first-out method (LIFO) cost allocation method, with perpetual inventory updating, to calculate (a) sales revenue, (b) cost of goods sold, and c) gross margin for B75 Company, considering the following transactions.arrow_forward

- Perpetual inventory using LIFO The following units of a particular item were available for sale during the calendar year: Jan. 1 Inventory 3,900 units at $41 Apr. 19 Sale 2,600 units June 30 Purchase 4,900 units at $46 Sept. 2 Sale 5,600 units Nov. 15 Purchase 2,000 units at $48 This information has been collected in the Microsoft Excel Online file. Open the spreadsheet, perform the required analysis, and input your answers in the question below. Open spreadsheet The firm maintains a perpetual inventory system. Determine the cost of goods sold for each sale and the inventory balance after each sale, assuming the last-in, first-out method. Present the data in the form illustrated in Exhibit 4. Under LIFO, if units are in inventory at two or more different costs, enter the units with the LOWER unit cost first in the Inventory Unit Cost column. Round your answers for quantity values to the nearest whole number, for unit cost values to the nearest cent, and for total cost values to the…arrow_forwardMusicPlace specializes in sound equipment. Company records indicate the following data for a line of speakers (Click the icon to view the data) Read the requirements Requirement 1. Determine the amounts that MusicPlace should report for cost of goods sold and ending inventory two ways: a. FIFO and b. LIFO (MusicPlace uses a perpetual inventory system.) Start by determining the amounts that MusicPlace should report for cost of goods sold and ending inventory under a FIFO FIFO method cost of goods sold FIFO method ending inventory Determinie the amounts that MusicPlace should report for cost of goods sold and ending inventory under b. LIFO. LIFO method cost of goods sold LIFO method ending inventory Requirement 2. MusicPlace uses the FIFO method. Prepare the company's income statement for the month ended March 31, 2021, reporting gross profit. Operating expenses totaled $280, and the income tax rate was 40%. (Round answers to the nearest dollar) MusicPlace Income Statement Month Ended…arrow_forwardAssume that Whitewall Tire Store completed the following perpetual inventory transactions for a line of tires: (Click the icon to view the transactions.) Requirement 1. Compute cost of goods sold and gross profit using the FIFO inventory costing method. Begin by computing the cost of goods sold and cost of ending merchandise inventory using the FIFO inventory costing method. Enter the transactions in chronological order, calculating new inventory on hand balances after each transaction. Once all of the transactions have been entered into the perpetual record, calculate the quantity and total cost of merchandise inventory purchased, sold, and on hand at the end of the period. (Enter the oldest inventory layers first.) Cost of Goods Sold Date Quantity Dec. 1 11 23 26 29 Totals Purchases Unit Cost Total Unit Cost Quantity Cost Total Cost Inventory on Hand Unit Cost Quantity C Total Cost 1. Requirements More info Dec. 1 Beginning merchandise inventory Dec. 11 Purchase Dec. 23 Sale Dec. 26…arrow_forward

- Assume that AB Tire Store completed the following perpetual inventory transactions for a line of tires: (Click the icon to view the transactions.) Requirements 1. 2. 3. 4. Compute cost of goods sold and gross profit using the FIFO inventory costing method. Compute cost of goods sold and gross profit using the LIFO inventory costing method. Compute cost of goods sold and gross profit using the weighted-average inventory costing method. (Round weighted-average cost per unit to the nearest cent and all other amounts to the nearest dollar.) Which method results in the largest gross profit, and why? X More info 4 Dec. 1 Beginning merchandise inventory Dec. 11 Purchase Dec. 23 Sale Dec. 26 Purchase Dec. 29 Sale 24 tires @ $61 each 6 tires @ $76 each 16 tires @ $83 each 14 tires @ $86 each 17 tires @ $83 eacharrow_forwardA home improvement store, like Lowe’s, carries the following items:Required:1. Compute the total cost of inventory.2. Determine whether each inventory item would be reported at cost or net realizable value. Multiply the quantity of each inventory item by the appropriate cost or NRV amount and place the total in the “Lower of Cost and NRV” column. Then determine the total of that column.3. Compare your answers in requirement 1 and requirement 2 and then record any necessary adjustment to write down inventory from cost to net realizable value.4. Discuss the financial statement effects of using lower of cost and net realizable value to report inventory.arrow_forwardFlora's Gifts reported the following current-month data for its only product. The company uses a periodic inventory system, and its ending inventory consists of 72 units-56 units from the January 6 purchase and 16 units from the January 25 purchase. January 1 Beginning inventory January 6 Purchase January 17 Purchase January 25 Purchase Totals 165 units@ $4.00 334 units @ $3.50 570 units @ $3.10 28 units @ $2.60 1,097 units = $ 660.00 1,169.00 1,767.00 72.80 $ 3,668.80 (a-d) Determine the cost assigned to ending inventory and to cost of goods sold for the following. (e) Which method yields the lowest net income?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,  Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Cengage Learning

College Accounting, Chapters 1-27

Accounting

ISBN:9781337794756

Author:HEINTZ, James A.

Publisher:Cengage Learning,

Financial Accounting

Accounting

ISBN:9781337272124

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:9781947172685

Author:OpenStax

Publisher:OpenStax College

Chapter 6 Merchandise Inventory; Author: Vicki Stewart;https://www.youtube.com/watch?v=DnrcQLD2yKU;License: Standard YouTube License, CC-BY

Accounting for Merchandising Operations Recording Purchases of Merchandise; Author: Socrat Ghadban;https://www.youtube.com/watch?v=iQp5UoYpG20;License: Standard Youtube License