Individual Income Taxes

43rd Edition

ISBN: 9780357109731

Author: Hoffman

Publisher: CENGAGE LEARNING - CONSIGNMENT

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 6, Problem 38P

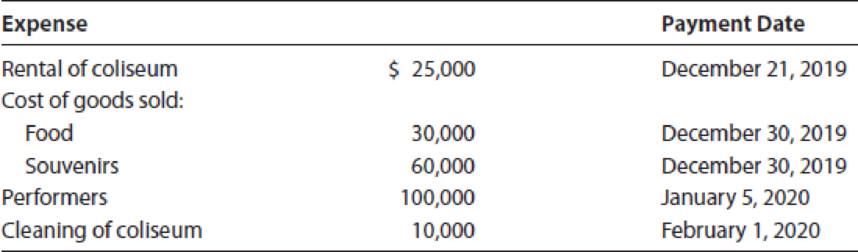

Duck, an accrual basis corporation, sponsored a rock concert on December 29, 2019. Gross receipts were $300,000. The following expenses were incurred and paid as indicated:

Because the coliseum was not scheduled to be used again until January 15, the company with which Duck had contracted did not perform the cleanup until January 8–10, 2020.

- a. Calculate Duck’s net income from the concert for tax purposes for 2019.

- b. Using the present value tables in Appendix H, what is the true cost to Duck if it had to defer the $100,000 deduction for the performers until 2020? Assume a 5% discount rate and a 21% marginal tax rate in 2019 and 2020.

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

1. During the year ended December 31, 2021, management of

Alpha Corporation (the Company) decided to sell a piece of

its idle equipment. The equipment had an original tax cost

of $75,000 and as of December 31, 2020, tax depreciation

of $75,000 had been taken on the equipment. The

equipment was sold to an unrelated party for $95,000 cash

on June 15, 2021. For the purpose of requirement 3, assume

that the book cost and book depreciation have been the

same as the tax cost and tax depreciation.

Required:

1. Calculate the tax gain on sale of the equipment.

2. Calculate the portion of the gain that is depreciation

recapture.

3. Prepare the journal entry to record sale of the equipment.

On January 1, 2021, Sheridan, Inc. purchased a machine for $2180000 which will be depreciated $218000 per year for financial statement reporting purposes. For income tax reporting, Sheridan elected to expense $243000 and to use straight-line depreciation which will allow a cost recovery deduction of $193000 for 2021. Assume a present and future enacted income tax rate of 20%. What amount should be added to Sheridan's deferred income tax liability for this temporary difference at December 31, 2021?

You are provided the following transactions which occurred during the tax year which 31 December 2022 for Serowe Ltd.

The company disposed some of its Heavy Plant and Machinery that it had bought on 30 November 2020 for P1,200,000. The company received P350,000. Serowe Ltd bought new Plant and Machinery to replace the disposed ones for P3,200,000.

Assume that the company elects to apply rollover relief, calculate the capital allowances on the new plant and machinery for the current tax year.

Chapter 6 Solutions

Individual Income Taxes

Ch. 6 - Prob. 1DQCh. 6 - Prob. 2DQCh. 6 - Classify each of the following expenditures paid...Ch. 6 - Prob. 4DQCh. 6 - Prob. 5DQCh. 6 - Prob. 6DQCh. 6 - Prob. 7DQCh. 6 - Prob. 8DQCh. 6 - Prob. 9DQCh. 6 - Prob. 10DQ

Ch. 6 - Prob. 11DQCh. 6 - Prob. 12DQCh. 6 - Prob. 13DQCh. 6 - Prob. 14DQCh. 6 - Linda operates an illegal gambling operation....Ch. 6 - Prob. 16DQCh. 6 - Melissa, the owner of a sole proprietorship, does...Ch. 6 - Prob. 18DQCh. 6 - Blaze operates a restaurant in Cleveland. He...Ch. 6 - Prob. 20DQCh. 6 - Prob. 21DQCh. 6 - Ray loses his job as a result of a corporate...Ch. 6 - Lavinia incurs various legal fees in obtaining a...Ch. 6 - Prob. 24DQCh. 6 - Prob. 25DQCh. 6 - Shanna, a calendar year and cash basis taxpayer,...Ch. 6 - Prob. 27CECh. 6 - Maud, a calendar year taxpayer, is the owner of a...Ch. 6 - Vella owns and operates an illegal gambling...Ch. 6 - Printer Company pays a 25,000 annual membership...Ch. 6 - Stanford owns and operates two dry cleaning...Ch. 6 - Tobias has a brokerage account and buys on the...Ch. 6 - Prob. 33PCh. 6 - Prob. 34PCh. 6 - Janice, age 32, earns 50,000 working in 2019. She...Ch. 6 - Prob. 36PCh. 6 - Prob. 37PCh. 6 - Duck, an accrual basis corporation, sponsored a...Ch. 6 - Prob. 39PCh. 6 - Prob. 40PCh. 6 - Prob. 41PCh. 6 - Prob. 42PCh. 6 - Terry traveled to a neighboring state to...Ch. 6 - Prob. 44PCh. 6 - Prob. 45PCh. 6 - Prob. 46PCh. 6 - Prob. 47PCh. 6 - Prob. 48PCh. 6 - Prob. 49PCh. 6 - Prob. 50PCh. 6 - Prob. 51PCh. 6 - Brittany Callihan sold stock (basis of 184,000) to...Ch. 6 - Prob. 53PCh. 6 - Prob. 54PCh. 6 - Prob. 55PCh. 6 - Prob. 56PCh. 6 - Prob. 57CPCh. 6 - Prob. 58CPCh. 6 - Prob. 1RPCh. 6 - Prob. 2RPCh. 6 - Prob. 3RPCh. 6 - Which of the following is a deduction for AGI? a....Ch. 6 - Which of the following is not a deduction for AGI?...Ch. 6 - David is a CPA and enjoys playing the lottery....Ch. 6 - Prob. 4CPACh. 6 - Prob. 5CPACh. 6 - Prob. 6CPA

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Ayres Services acquired an asset for $200 million in 2021. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 25%. Amounts for pretax accounting income, depreciation, and taxable income in 2021, 2022, 2023, and 2024 are as follows: 2021 $405 $425 ($ in millions) 2022 2023 2024 $440 Pretax accounting income Depreciation on the income statement Depreciation on the tax return $475 50 50 50 50 (64) (84) (30) (22) Taxable income $391 $391 $460 $503 Required: For December 31 of each year, determine (a) the cumulative temporary book-tax difference for the depreciable asset and (b) the balance to be reported in the deferred tax liability account. (Leave no cell blank, enter "O" wherever applicable. Enter your answers in millions rounded to 2 decimal place (i.e., 5,500,000 should be entered as 5.50).) Beginning of End of 2021 End of End of End…arrow_forwardAyres Services acquired an asset for $144 million in 2021. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset/s cost is depreciated by MACRS. The enacted tax rate is 25%. Amounts for pretax accounting income, depreciation, and taxable income in 2021, 2022, 2023, and 2024 are as follows: _ ($ in millions) ____________ 2021 2022 2023 2024 Pretax accounting income $370 $390 $405 $440 Depreciation on the income statement 36 36 36 36 Depreciation on the tax return (57) (49) (23) (15) Taxable income…arrow_forwardDoxon Development began operations in December 2021. When lots for industrial development are sold, Dixon recognizes income for financial reporting purposes in the year of the sale. For some lots, Dixon recognizes income for tax purposes when collected. Income recognized for financial reporting purposes in 2021 for lots sold this way was $14 million, which wili be collected over the next three years Scheduled collections for 2022-2024 are as follows $4 nillion 6 million 4 nillion $ 14 million 2022 2023 2024 Pretax accounting income for 2021 was $19 milion. The enacted tax rate is 30% Required: 1. Assuming no differences between accounting income and taxable income other than those described above, prepare the journal entry to record income taxes in 2021. 2. Suppose a new tax law, revising the tax rate from 30% to 25%, beginning in 2023, is enacted in 2022, when pretax accounting Income was $16 million. No 2022 lot sales qualified for the special tax treatment. Prepare the appropriate…arrow_forward

- Ayres Services acquired an asset for $128 million in 2021. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset’s cost is depreciated by MACRS. The enacted tax rate is 25%. Amounts for pretax accounting income, depreciation, and taxable income in 2021, 2022, 2023, and 2024 are as follows: ($ in millions) 2021 2022 2023 2024 Pretax accounting income $ 360 $ 380 $ 395 $ 430 Depreciation on the income statement 32 32 32 32 Depreciation on the tax return (55 ) (39 ) (21 ) (13 ) Taxable income $ 337 $ 373 $ 406 $ 449 Required:For December 31 of each year, determine (a) the cumulative temporary book-tax difference for the depreciable asset and (b) the balance to be reported in the deferred tax liability account. (Leave no cell blank, enter "0" wherever applicable. Enter your answers in millions…arrow_forwardAyres Services acquired an asset for $168 million in 2021. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset’s cost is depreciated by MACRS. The enacted tax rate is 25%. Amounts for pretax accounting income, depreciation, and taxable income in 2021, 2022, 2023, and 2024 are as follows: ($ in millions) 2021 2022 2023 2024 Pretax accounting income $ 385 $ 405 $ 420 $ 455 Depreciation on the income statement 42 42 42 42 Depreciation on the tax return (60 ) (64 ) (26 ) (18 ) Taxable income $ 367 $ 383 $ 436 $ 479 Required:For December 31 of each year, determine (a) the cumulative temporary book-tax difference for the depreciable asset and (b) the balance to be reported in the deferred tax liability account. Beginning of 2021 End of 2021 End of 2022 End of 2023 End of 2024 Cumulative…arrow_forwardA company acquired an asset for $1,200,000 in 2024. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 19%. Amounts for pretax accounting income, depreciation, and taxable income in 2024, 2025, 2026, and 2027 are as follows: Asset's Cost Useful life Enacted tax rate Pretax accounting income Depreciation on the income statement Depreciation on the tax return Taxable income Required: Cumulative Temporary Difference Deferred Tax Liability Jan. 1, 2024 $1,200,000 $0 0 4 years 19% 2024 $3,700,000 300,000 (399,960) $3,600,040 2025 $4,100,000 300,000 (533,400) $3,866,600 For December 31 of each year, determine (a) the cumulative temporary book-tax difference for the depreciable asset and (b) the balance to be reported in the deferred tax liability account. Each cell requires a formula, even if the result is $0. 2026 $4,400,000 300,000…arrow_forward

- Ayres Services acquired an asset for $82 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: Pretax accounting income Depreciation on the income statement Depreciation on the tax return. Taxable income. ($ in millions) 2019 355 $ 20.5 (33.5) Temporary Difference Deferred Tax Liability 2018 $ 335 $ 20.5 (25.5) $ 330 $ 342 $ 375 2020 2021 370 $ 405 20.5 20.5 (15.5) (7.5) $ 418 Required: Determine (a) the temporary book-tax difference for the depreciable asset and (b) the balance to be reported in the deferred tax liability account. (Leave no cell blank, enter "0" wherever applicable. Show all amounts as positive amounts. Enter your answers in millions rounded to 1 decimal place (i.e., 5,500,000 should…arrow_forwardIn 2021, Crane Company accrued, for financial statement reporting, estimated losses on disposal of unused plant facilities of $3710000. The facilities were sold in March 2022 and a $3710000 loss was recognized for tax purposes. Also in 2021, Crane paid $163200 in premiums for a two-year life insurance policy in which the company was the beneficiary. Assuming that the enacted tax rate is 20% in both 2021 and 2022, and that Crane paid $1280000 in income taxes in 2021, the amount reported as net deferred income taxes on Crane's balance sheet at December 31, 2021, should be a $371000 liability. $742000 asset. $1116800 asset. $371000 asset.arrow_forwardAt the beginning of 2018, FECC Corporation had discovered that the depreciation expense inthe years prior to 2018 was incorrectly calculated and recorded. For the years before 2018,total depreciation expense of $165,000 was recorded, whereas correct total depreciationexpense was $75,000. The tax rate is 30%. FECC follows IFRS and the deferred taxes method ofaccounting for income taxes.Required:1) Prepare FECC’s 2017 journal entry with respect to the depreciation expense that wasrecorded in the years prior to 2018.arrow_forward

- Ayres Services acquired an asset for $80 million in 2024. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 25%. Amounts for pretax accounting income, depreciation, and taxable income in 2024, 2025, 2026, and 2027 are as follows: Pretax accounting income Depreciation on the income statement Depreciation on the tax return Taxable income Required: 2024 $ 330 20 (25) $325 Cumulative Temporary Difference Deferred Tax Liability ($ in millions) 2025 $350 20 (33) $337 2026 $365 20 (15) $370 $413 Beginning of 2024 2027 $ 400 For December 31 of each year, determine (a) the cumulative temporary book-tax difference for the depreciable asset and (b) the balance to be reported in the deferred tax liability account. Note: Leave no cell blank, enter "0" wherever applicable. Enter your answers in millions rounded to 2 decimal places (i.e., 5,500,000…arrow_forwardIn 2025, Sheridan Company accrued, for financial statement reporting, estimated losses on disposal of unused plant facilities of $3650000. The facilities were sold in March 2026 and a $3650000 loss was recognized for tax purposes. Also in 2025, Sheridan paid $156000 in premiums for a two-year life insurance policy in which the company was the beneficiary. Assuming that the enacted tax rate is 20% in both 2025 and 2026 and that Sheridan paid $1220000 in income taxes in 2025, the amount reported as net deferred income taxes on Sheridan's balance sheet at December 31, 2025, should be a O $698800 asset. O $365000 asset. O $365000 liability. O $730000 asset.arrow_forwardAyres Services acquired an asset for $116 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: (S in millions) 2019 $ 420 $ 440 $ 455 29.0 2018 2020 2021 $ 490 Pretax accounting income Depreciation on the income statement Depreciation on the tax return 29.0 29.0 29.0 (34.0) (42.0) (24.0) 415 $ 427 (16.0) $ 503 Taxable income $ 460 Required: Determine (a) the temporary book-tax difference for the depreciable asset and (b) the balance to be reported in the deferred tax liability account. (Leave no cell blank, enter "0" wherever applicable. Show all amounts as positive amounts. Enter your answers in millions rounded to 1 decimal place (i.e., 5,500,000 should be entered as 5.5).) Beginning of 2018 End of…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income Taxes

Accounting

ISBN:9780357109731

Author:Hoffman

Publisher:CENGAGE LEARNING - CONSIGNMENT

Depreciation -MACRS; Author: Ronald Moy, Ph.D., CFA, CFP;https://www.youtube.com/watch?v=jsf7NCnkAmk;License: Standard Youtube License