Concept explainers

Videos

Problem 3-70B Comprehensive Problem: Reviewing the Accounting Cycle

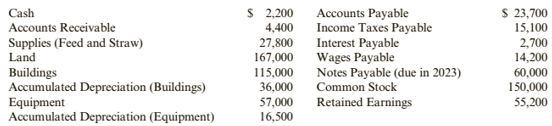

Wilburton Riding Stables provides stables, care for animals, and grounds for riding and showing horses. The account balances at the beginning of 2019 were:

During 2019, the following transactions occurred:

- Wilburton provided animal care services, all on credit, for $210,300. Wilburton rented stables to customers for $20,500 cash. Wilburton rented its grounds to individual riders, groups, and show organizations for $41,800 cash.

- There remains $15,600 of

accounts receivable to be collected at December 31, 2019. - Feed in the amount of $62,900 was purchased on credit and debited to the supplies

- Straw was purchased for $7,400 cash and debited to the supplies account.

- Wages payable at the beginning of 2019 were paid early in 2019. Wages were earned and paid during 2019 in the amount of $12,000.

- The income taxes payable at the beginning of 2019 were paid early in 2019.

- Payments of $73,000 were made to creditors for supplies previously purchased on credit.

- One year’s interest at 9% was paid on the note payable on July 1, 2019.

- During 2019, Jon Wilburton, a principal stockholder, purchased a horse for his Wife, Jennifer, to ride. The horse cost $7,000, and Wilburton used his personal credit to purchase it. The horse is stabled at the Wilburton home rather than at the riding stables.

- Property taxes were paid on the land and buildings in the amount of S17,000.

- Dividends were declared and paid in the amount Of

The following data are available for

• Supplies (feed and straw) in the amount of $30,400 remained at year end.

• Annual depreciation on the buildings is $6,000.

• Annual depreciation on the equipment is

• Wages of $4,000 were unrecorded and unpaid at year end.

• Interest for 6 months at 9% per year on the note is unpaid and unrecorded at year end.

• Income taxes of $16,500 were unpaid and unrecorded at year end.

Required:

- Post the 2019 beginning balances to T-accounts. Prepare

journal entries for Transactions a through k andpost the journal entries to T-accounts, adding any new T-accounts you need. - Prepare the adjustments and post the adjustments to the T-accounts, adding any new T-accounts you need.

- Prepare an income statement.

- Prepare a

retained earnings statement. - Prepare a classified balance sheet.

- Prepare closing entries.

- CONCEPTUAL CONNECTION Did you include Transaction i among Wilburton’s 2019 journal entries? Why or why not?

1.

To record: Journal entries and prepare T accounts to post those entries.

Introduction: Journal entries provide a record of the financial activities undertaken within an organization. Journal entries helps in preparation of financial statements of a company.

Explanation of Solution

Journalizing:

Journalizing is the process of recording the transactions of an organization in a chronological order. Based on these journal entries recorded, the accounts are posted to the relevant ledger accounts.

Accounting rules for journal entries:

- To increase balance of the account: Debit assets, expenses, losses and credit all liabilities, capital, revenue and gains.

- To decrease balance of the account: Credit assets, expenses, losses and debit all liabilities, capital, revenue and gains.

Recording service revenue:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Accounts receivables | 210,300 | |||

| Care service | 210,300 | |||

| (to record service revenue) |

Table (1)

- Since accounts receivables is an asset and asset is increased. Hence, accounts receivablesaccount is debited.

- Since care service is an income and income is increased. Hence, care service account is credited.

Recording service revenue:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Cash | 62,300 | |||

| Stable rent service | 20,500 | |||

| Ground rent service | 41,800 | |||

| (to record service revenue) |

Table (2)

- Since cash is an asset and asset is increased. Hence, cash account is debited.

- Since stable rent service is an income and income is increased. Hence, stable rent service account is credited.

- Since ground rent service is an income and income is increased. Hence, ground rent service account is credited.

Recording receipt from accounts receivables:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Cash | 199,100 | |||

| Accounts receivable | 199,100 | |||

| (to record receipt of accounts receivables) |

Table (3)

- Since cash is an asset and asset is increased. Hence, cash account is debited.

- Since accounts receivables is an asset and asset is decreased. Hence, accounts receivables is credited.

Recording purchase of supplies:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Supplies | 62,900 | |||

| Accounts payable | 62,900 | |||

| (to record purchase of supplies) |

Table (4)

- Since supplies is an asset and asset is increased. Hence, supplies account is debited.

- Since accounts payable is a liability and liability is increased. Hence, accounts payable is credited.

Recording purchase of supplies:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Supplies | 7,400 | |||

| Cash | 7,400 | |||

| (to record purchase of supplies) |

Table (5)

- Since supplies is an asset and asset is increased. Hence, supplies account is debited.

- Since cash is an asset and asset is decreased. Hence, cashaccount is credited.

Recording cash paid for wages:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Wages payable | 14,200 | |||

| Wages expense | 112,000 | |||

| Cash | 126,200 | |||

| (to record payment of wages) |

Table (6)

- Since wages payable is a liability and liability is decreased. Hence, wages payable account is debited.

- Since wages expense is an expense and expense is increased. Hence, wages expense account is debited.

- Since cash is an asset and asset is decreased. Hence, cash account is credited.

Recording repayment of income tax payable:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Income tax payable | 15,100 | |||

| Cash | 15,100 | |||

| (to record payment of income tax) |

Table (7)

- Since income tax payable is a liability and liability is decreased. Hence, income tax payable account is debited.

- Since cash is an asset and asset is decreased. Hence, cash account is credited.

Recording repayment of accounts payable:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Accounts payable | 73,000 | |||

| Cash | 73,000 | |||

| (to record repayment of accounts payable) |

Table (8)

- Since accounts payable is a liability and liability is decreased. Hence, accounts payableaccount is debited.

- Since cash is an asset and asset is decreased. Hence, cash account is credited.

Recording payment of interest on notes payable:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Interest expense | 2,700 | |||

| Interest payable | 2,700 | |||

| Cash | 5,400 | |||

| (to record interest payment) |

Table (9)

- Since interest expense is an expense and expense is increased. Hence, interest expenseaccount is debited.

- Since interest payable is a liability and liability is decreased. Hence, interest payableaccount is debited.

- Since cash is an asset and asset is decreased. Hence, cash account is credited.

Recording withdrawal of cash for personal purposes:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Drawings | 7,000 | |||

| Cash | 7,000 | |||

| (to record drawing) |

Table (10)

- Since drawing is capital and capital is decreased. Hence, drawing account is debited.

- Since cash is an asset and asset is decreased. Hence, cash account is credited.

Recording property taxes:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Property taxes | 17,000 | |||

| Cash | 17,000 | |||

| (to record property taxes) |

Table (11)

- Since property taxes is an expense and expense is increased. Hence, property taxes account is debited.

- Since cash is an asset and asset is decreased. Hence, cash account is credited.

Recording dividend payment:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Dividend | 7,200 | |||

| Cash | 7,200 | |||

| (to record dividend payment) |

Table (12)

- Since dividend is an expense and expense is increased. Hence, dividend account is debited.

- Since cash is an asset and asset is decreased. Hence, cash account is credited.

Working Notes:

Computation of cash received from accounts receivables:

Preparation of cash account in general ledger:

| Cash | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 2,200 | 2,200 | |||

| Stable rent service | 20,500 | 22,700 | |||

| Ground rent service | 41,800 | 64,500 | |||

| Accounts receivable | 199,100 | 263,600 | |||

| Supplies | 7,400 | 256,200 | |||

| Wages payable | 14,200 | 242,000 | |||

| Wages expenses | 112,000 | 130,000 | |||

| Income tax payable | 15,100 | 114,900 | |||

| Accounts payable | 73,000 | 41,900 | |||

| Interest expense | 2,700 | 39,200 | |||

| Interest payable | 2,700 | 36,500 | |||

| Drawings | 7,000 | 29,500 | |||

| Property tax | 17,000 | 12,500 | |||

| Dividend | 7,200 | 5,300 | |||

Table (13)

Preparation of accounts receivable account in general ledger:

| Accounts receivable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 4,400 | ||||

| Care service | 210,300 | 214,700 | |||

| Cash | 199,100 | 15,600 | |||

Table (14)

Preparation of supplies account in general ledger:

| Supplies | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 27,800 | ||||

| Accounts payable | 62,900 | 90,700 | |||

| Cash | 7,400 | 98,100 | |||

Table (15)

Preparation of land account in general ledger:

| Land | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 167,000 | ||||

Table (16)

Preparation of building account in general ledger:

| Building | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 115,000 | ||||

Table (17)

Preparation of accumulated depreciation account in general ledger:

| Accumulated depreciation-Building | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

Table (18)

Preparation of equipment account in general ledger:

| Equipment | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 57,000 | ||||

Table (19)

Preparation of accumulated depreciation account in general ledger:

| Accumulated depreciation-Equipment | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

Table (20)

Preparation of accounts payable account in general ledger:

| Accounts payable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

| Supplies | 62,900 | ||||

| Cash | 73,000 | ||||

Table (21)

Preparation of income tax payable account in general ledger:

| Income tax payable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

| Cash | 15,100 | 0 | |||

Table (22)

Preparation of interest payable account in general ledger:

| Interest payable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

| Cash | 2,700 | 0 | |||

Table (23)

Preparation of wages payable account in general ledger:

| Wages payable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

| Cash | 14,200 | 0 | |||

Table (24)

Preparation of notes payable account in general ledger:

| Notes payable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

Table (25)

Preparation of common stock account in general ledger:

| Common stock | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

Table (26)

Preparation of retained earnings account in general ledger:

| Retained earnings | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

Table (27)

Preparation of Care service account in general ledger:

| Care service | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Accounts receivable | 210,300 | ||||

Table (28)

Preparation of Stables rentservice account in general ledger:

| Stables rent service | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 20,500 | ||||

Table (29)

Preparation of ground rent service account in general ledger:

| Ground rent service | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 41,800 | ||||

Table (30)

Preparation of wages expense account in general ledger:

| Wages expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 112,000 | 112,000 | |||

Table (31)

Preparation of drawing account in general ledger:

| Drawing | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 7,000 | 7,000 | |||

Table (32)

Preparation of interest expense account in general ledger:

| Interest expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 2,700 | 2,700 | |||

Table (33)

Preparation of property tax account in general ledger:

| Property tax expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 17,000 | 17,000 | |||

Table (34)

Preparation of dividend account in general ledger:

| Dividend expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 7,200 | 7,200 | |||

Table (35)

2.

To record: Adjusting entries. Also, post the adjustment entries in the respective T accounts.

Introduction: Adjusting entries are made at the end of reporting period at the time of preparation of financial statements. Adjusting entries are recorded to reflect the correct picture of financial position of the organization in the financial statements.

Explanation of Solution

Recording adjustment of supplies:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Supplies Expense | 67,700 | |||

| Supplies | 67,700 | |||

| (to record adjustment of supplies) |

Table (36)

- Since supplies expense is an expense and expense is increased. Hence, supplies expense account is debited.

- Since supplies is an asset and asset is decreased. Hence, supplies account is credited.

Recording depreciation expense:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Depreciation -Building | 6,000 | |||

| Accumulated depreciation-Building | 6,000 | |||

| (to record depreciation expense) |

Table (37)

- Since depreciation is an expense and expense is increased. Hence, depreciation-Building account is debited.

- Since accumulated depreciation is a contra asset and contra asset is increased. Hence, accumulated depreciation-Building account is credited.

Recording depreciation expense:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Depreciation -Equipment | 5,500 | |||

| Accumulated depreciation-Equipment | 5,500 | |||

| (to record depreciation expense) |

Table (38)

- Since depreciation is an expense and expense is increased. Hence, depreciation-Equipment account is debited.

- Since accumulated depreciation is a contra asset and contra asset is increased. Hence, accumulated depreciation-Equipment account is credited.

Recording wages payable:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Wages expense | 4,000 | |||

| Wages payable | 4,000 | |||

| (to record wages expense) |

Table (39)

- Since wages expense is an expense and expense is increased. Hence, wages expense account is debited.

- Since wages payable is a liability and liability is increased. Hence, wages payable account is credited.

Recording interest expense:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Interest expense | 2,700 | |||

| Interest Payable | 2,700 | |||

| (to record interest expense) |

Table (40)

- Since interestexpense is an expense and expense is increased. Hence, interestexpense account is debited.

- Since interest payable is a liability and liability is increased. Hence, interest payable account is credited.

Recording income tax expense:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Income tax expense | 16,500 | |||

| Income tax payable | 16,500 | |||

| (to record income tax expense) |

Table (41)

- Since income tax is an expense and expense is increased. Hence, income tax account is debited.

- Since income tax payable is a liability and liability is increased. Hence, income tax payable account is credited.

Working Note:

Computation of interest payable:

Preparation of cash account in general ledger:

| Cash | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 2,200 | 2,200 | |||

| Stable rent service | 20,500 | 22,700 | |||

| Ground rent service | 41,800 | 64,500 | |||

| Accounts receivable | 199,100 | 263,600 | |||

| Supplies | 7,400 | 256,200 | |||

| Wages payable | 14,200 | 242,000 | |||

| Wages expenses | 112,000 | 130,000 | |||

| Income tax payable | 15,100 | 114,900 | |||

| Accounts payable | 73,000 | 41,900 | |||

| Interest expense | 2,700 | 39,200 | |||

| Interest payable | 2,700 | 36,500 | |||

| Drawings | 7,000 | 29,500 | |||

| Property tax | 17,000 | 12,500 | |||

| Dividend | 7,200 | 5,300 | |||

Table (42)

Preparation of accounts receivable account in general ledger:

| Accounts receivable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 4,400 | ||||

| Care service | 210,300 | 214,700 | |||

| Cash | 199,100 | 15,600 | |||

Table (43)

Preparation of supplies account in general ledger:

| Supplies | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 27,800 | ||||

| Accounts payable | 62,900 | 90,700 | |||

| Cash | 7,400 | 98,100 | |||

| Supplies expense | 67,700 | 30,400 | |||

Table (44)

Preparation of land account in general ledger:

| Land | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 167,000 | ||||

Table (45)

Preparation of building account in general ledger:

| Building | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 115,000 | ||||

Table (46)

Preparation of accumulated depreciation account in general ledger:

| Accumulated depreciation-Building | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

| Depreciation-building | 6,000 | ||||

Table (47)

Preparation of equipment account in general ledger:

| Equipment | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | 57,000 | ||||

Table (48)

Preparation of accumulated depreciation account in general ledger:

| Accumulated depreciation-Equipment | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

| Depreciation-equipment | 5,500 | ||||

Table (49)

Preparation of accounts payable account in general ledger:

| Accounts payable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

| Supplies | 62,900 | ||||

| Cash | 73,000 | ||||

Table (50)

Preparation of income tax payable account in general ledger:

| Income tax payable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

| Cash | 15,100 | 0 | |||

| Income tax expense | 16,500 | ||||

Table (51)

Preparation of interest payable account in general ledger:

| Interest payable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

| Cash | 2,700 | 0 | |||

| Interest expense | 2,700 | ||||

Table (52)

Preparation of wages payable account in general ledger:

| Wages payable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

| Cash | 14,200 | 0 | |||

| Wages expense | 4,000 | ||||

Table (53)

Preparation of notes payable account in general ledger:

| Notes payable | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

Table (54)

Preparation of common stock account in general ledger:

| Common stock | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

Table (55)

Preparation of retained earnings account in general ledger:

| Retained earnings | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Balance | |||||

Table (56)

Preparation of Care service account in general ledger:

| Care service | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Accounts receivable | 210,300 | ||||

Table (57)

Preparation of Stables rentservice account in general ledger:

| Stables rent service | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 20,500 | ||||

Table (58)

Preparation of ground rent service account in general ledger:

| Ground rent service | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 41,800 | ||||

Table (59)

Preparation of wages expense account in general ledger:

| Wages expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 112,000 | 112,000 | |||

| Wages payable | 4,000 | 116,000 | |||

Table (60)

Preparation of drawing account in general ledger:

| Drawing | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 7,000 | 7,000 | |||

Table (61)

Preparation of interest expense account in general ledger:

| Interest expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 2,700 | 2,700 | |||

| Interest payable | 2,700 | 5,400 | |||

Table (62)

Preparation of property tax account in general ledger:

| Property tax expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 17,000 | 17,000 | |||

Table (63)

Preparation of dividend account in general ledger:

| Dividend expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Cash | 7,200 | 7,200 | |||

Table (64)

Preparation of supplies expense in general ledger:

| Supplies expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Supplies | 67,700 | 67,700 | |||

Table (65)

Preparation of depreciation expense account in general ledger:

| Depreciation-building expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Accumulated depreciation-building | 6,000 | 6,000 | |||

Table (66)

Preparation of depreciation expense account in general ledger:

| Depreciation-equipment expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Accumulated depreciation-equipment | 5,500 | 5,500 | |||

Table (67)

Preparation of income tax expense account in general ledger:

| Income tax expense | |||||

| Date | Particular | Post Ref. | Debit($) | Credit($) | Balance($) |

| Income tax payable | 16,500 | 16,500 | |||

Table (68)

3.

To prepare: Income statement.

Introduction: Income statement is prepared to ascertain net income of a company for a period. Net income shows operating efficiency of a company.

Explanation of Solution

Preparation of income statement for the year ending 31st December,2019:

| CompanyA | ||

| Income Statement | ||

| Amount ($) | Amount ($) | |

| Revenues: | ||

| Care service | 210,300 | |

| Stables rent service | 20,500 | |

| Ground rent service | 41,800 | |

| Total Revenue | 272,600 | |

| Expenses: | ||

| Wages expense | 116,000 | |

| Interest expense | 5,400 | |

| Supplies expense | 67,700 | |

| Property tax | 17,000 | |

| Depreciation-building expense | 6,000 | |

| Depreciation-equipment expense | 5,500 | |

| Income tax expense | 16,500 | |

| Total Expenses | 234,100 | |

| Net Income | 38,500 | |

Table (69)

4.

To prepare: Statement of retained earnings.

Introduction: Statement of retained earnings shows the net impact on retained earnings of the company, in a given period.

Explanation of Solution

Preparation of statement of retained earnings as on 31st December,2019:

| Company A | ||

| Statement of Retained Earning | ||

| Amount($) | Amount($) | |

| Owner’s Equity opening balance | 55,200 | |

| Add: Capital introduced by owner | ||

| Add: Net income | 38,500 | |

| Total: | 93,700 | |

| Less: Withdrawals | ||

| Less: Dividend | ||

| Closing Balance | 79,500 | |

Table (70)

5.

To prepare: Balance sheet of the company at the end of the accounting period.

Introduction: Balance sheet shows the status of assets and liabilities of the company, in which total assets equates with total liabilities and equity.

Explanation of Solution

Preparation of balance sheet as on 31st December,2019:

| Company A | ||

| Balance Sheet | ||

| Amount ($) | Amount($) | |

| Liabilities and Owners Equity | ||

| Current Liabilities | ||

| Accounts Payable | 13,600 | |

| Wages Payable | 4,000 | |

| Interest Payable | 2,700 | |

| Income tax payable | 16,500 | |

| Total Current Liabilities | 36,800 | |

| Non-Current Liabilities | ||

| Note Payable (due in 2023) | 60,000 | |

| Total Non-Current Liabilities | 60,000 | |

| Total Liabilities | ||

| Common Stock | 150,000 | |

| Retained Earnings | 79,500 | 229,500 |

| Total Liabilities and Owner’s Equity | 326,300 | |

| Current Assets | ||

| Cash | 5,300 | |

| Accounts Receivable | 15,600 | |

| Supplies | 30,400 | |

| Total Current Assets | 51,300 | |

| Property, Plant and Equipment | ||

| Land | 167,000 | |

| Building | 115,000 | |

| Less: accumulated depreciation | ||

| Equipment | 57,000 | |

| Less: accumulated depreciation | ||

| Total Property, Plant and Equipment | 275,000 | |

| Total Assets | 326,300 | |

Table (71)

6.

To record: closing journal entries.

Introduction: Closing entries are posted to close all the temporary accounts of the accounting books. Closing entries zeros the balances of income statement items, drawings, and dividends.

Explanation of Solution

Recording closing entry for expense accounts:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Income summary | 234,100 | |||

| Wages expense | 116,000 | |||

| Interest expense | 5,400 | |||

| Property tax expense | 17,000 | |||

| Supplies expense | 67,700 | |||

| Depreciation-building expense | 6,000 | |||

| Depreciation-equipment expense | 5,500 | |||

| Income tax expense | 16,500 | |||

| (to record closing of expense accounts) |

Table (72)

- Since income summary is a temporary income account and temporary income is decreased. Hence, income summary account is debited.

- Since wages expense is an expense and expense is decreased. Hence, wages expense account is credited.

- Since interest expense is an expense and expense is decreased. Hence, interest expense account is credited.

- Since property tax is an expense and expense is decreased. Hence, property tax account is credited.

- Since supplies expense is an expense and expense is decreased. Hence, supplies expense account is credited.

- Since depreceiation expense is an expense and expense is decreased. Hence, depreceiation -building expense account is credited.

- Since depreceiation expense is an expense and expense is decreased. Hence, depreceiation-equipment expense account is credited.

- Since income tax is an expense and expense is decreased. Hence, income tax account is credited.

Recording closing entry for revenue accounts:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Care service | 210,300 | |||

| Stables rent service | 20,500 | |||

| Ground rent service | 41,800 | |||

| Income summary | 272,600 | |||

| (to record closing of revenue account) |

Table (73)

- Since care service is an income and income is decreased. Hence, care service account is debited.

- Since stables rent service is an income and income is decreased. Hence, stables rent service account is debited.

- Since ground rent service is an income and income is decreased. Hence, ground rent serviceaccount is debited.

- Since income summary is a temporary income account and temporary income is increased. Hence, income summary account is credited.

Recording transfer of income summary account:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Income summary | 38,500 | |||

| Retained earnings | 38,500 | |||

| (to record closing entry) |

Table (74)

- Since income summary is a temporary income account and temporary income is decreased. Hence, income summary account is debited.

- Since retained earnings is a reserve and reserve is increased. Hence, retained earnings account is credited.

Transfering drawings and dividends to retained earnings:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Retained earnings | 14,200 | |||

| Drawings | 7,000 | |||

| Dividend | 7,200 | |||

| (to record closing entry) |

Table (75)

- Since retained earnings is a reserve and reserve is decreased. Hence, retained earnings account is debited.

- Since drawings is capital and capital is increased. Hence, drawingss account is credited.

- Since dividends is expense and expense is decreased. Hence, dividends account is credited.

7.

Whether the given transaction relating to personal expense should be recorded in the books or not.

Introduction: Personal expenses are incurred by the owners for their personal use by utilizing the resources of the company.

Explanation of Solution

Personal expenses should also be recorded in the books of the company because these expenses are incurred by using the cash of company. In case, such expenses are not included in the books then , cash account would not show the correct balance.

Personal expenses are shown as drawings by the owners and it is reduced from the owner’s funds. Therefore, it is necessary to record personal expenses, incurred by using the resources of company to show accurate and complete financial position.

Want to see more full solutions like this?

Chapter 3 Solutions

Cornerstones of Financial Accounting

- Notes Receivable Metzler Communications designs and programs a website for a local business. Metzler charges $46,000 for the project, and the local business signs an 8% note January 1, 2019. Required: 1. Prepare the journal entry to record the sale on January 1, 2019. 2. Determine how much interest Metzler will receive if the note is repaid on October 1, 2019. 3. Prepare Metzlers journal entry to record the cash received to pay off the note and interest on October 1, 2019.arrow_forwardBlue Company, an architectural firm, has a bookkeeper who maintains a cash receipts and disbursements journal. At the end of the year (2019), the company hires you to convert the cash receipts and disbursements into accrual basis revenues and expenses. The total cash receipts are summarized as follows. The accounts receivable from customers at the end of the year are 120,000. You note that the accounts receivable at the beginning of the year were 190,000. The cash sales included 30,000 of prepayments for services to be provided over the period January 1, 2019, through December 31, 2021. a. Compute the companys accrual basis gross income for 2019. b. Would you recommend that Blue use the cash method or the accrual method? Why? c. The company does not maintain an allowance for uncollectible accounts. Would you recommend that such an allowance be established for tax purposes? Explain.arrow_forwardd. Jasmine Perfume Bhd involves in manufacturing perfume-based products. On 25 June 2019, Jasmine Perfume Bhd had sold 30 boxes of its perfume-based products to NJ Sdn Bhd on credit. Required: 1) Explain whether the transaction occur on 25 June 2019 is an income to Jasmine Perfume Bhd.arrow_forward

- d. Get the totálš ar pr e. How much is the cash? Problem 2. Fay Fedor started a delivery service, Fed Deliveries, on July 1,2018 The following transactions occurred during the month of July: July 1 She contributed P 100,000 cash Purchased a used van for deliveries for P 120,000 by paying P 20,000 cash and signed a two-year notes payable for the remaining balance 3 Paid P 15,000 for office rent for the month Delivery services amounted to P 44,000. Half on account Cash of P 2,000 withdrawn by Fay 12 Purchased supplies for P 1,500 on account 15 Received cash of P 12,500 for services provided on July 5 17 Purchased gasoline for P 7,500 on account A globally competitive university for science, technology, and environmental conser2020.11.19 21:26 Development of a highly comnetitive human 2. 5. 91arrow_forwardDuring January 2020 Orgonite Wellness Clinic completed the following transactions : Jan 1 Orgonite received $ 50,000 cash and issued common shares to shareholders 4 Purchased supplies , $ 5,000 , and equipment , $ 2,500 on account 5 Performed checkup services , and received cash , $ 2,500 7 Paid cash to acquire land for an office site , $ 25,000 11 Performed a therapy session , and billed the customer $ 2500 16 Paid for the equipment , purchased Oct 4 on account 17 Paid the telephone bill , $ 150 18 Received partial payment from client on account , $ 2000 22 Paid the water and electricity bills , $ 500 29 Received $ 5,000 cash for conducting a workshop on " Healthy Living " 31 Paid employee salary , $ 4,000 31 Declared and paid dividends of $ 4,500 Requirements : Record each transaction in the journal . Key each transaction by date . Prepare the trial balance of Orgonite , at Jan 31 , 2020 .arrow_forwardAlpharack Company sells a line of tennis equipment to retailers. Alpharack uses the perpetualinventory system and engaged in the following transactions during April 2019, its first month of operations:a. On April 2, Alpharack purchased, on credit, 360 Wilbur T-100 tennis rackets with credit terms of 2/10, n/30. The rackets were purchased at a cost of $30 each. Alpharack paid Barker Trucking $195 to transport the tennis rackets from the manufacturer to Alpharack’s warehouse, shipping terms were F.O.B. shipping point, and the items were shipped on April 2.b. On April 3, Alpharack purchased, for cash, 115 packs of tennis balls for $10 per pack. c. On April 4, Alpharack purchased tennis clothing, on credit, from Designer Tennis Wear.The cost of the clothing was $8,250. Credit terms were 2/10, n/25.d. On April 10, Alpharack paid for the purchase of the tennis rackets in Transaction a.e. On April 15, Alpharack determined…arrow_forward

- Record any 5 accounting transactions of your own choice for furniture business for the year 2019, starting from the owner investment of $100,000. Post them in general journal,make ledger and trial balance for those entries.arrow_forwardPresented below are the transactions of Weirdo Beauty Salon for the month of January. 2020 Jan. 5 Received P25,500 from various customers as salon income 7 Purchased salon equipment on account, P7,500 8 Bought salon chairs and reception table from Plums Trading on account, P12,000 10 Returned defective chair to Plums Trading valued at P1,000 11 Made partial payment to Plums Trading P2,500 12 Purchased salon supplies paying P3,000 cash 15 The owner, Ms. Matutina, invested a table worth P1,750 Required: (a) Prepare the journal entries. (b) Prepare the T-Accounts.USE MS EXCEL AND SHOW FORMULAS USEDarrow_forwardEvery entry should have narration please Problem 1 November 19, 2020, BG Ltd purchased a mini excavator from an equipment supplier. The cost of the excavator was 560,000, with $6,000 paid in cash, and a note for $54.000 with interest on the note at 4% all due on November 18, 2021. BG Ltd. has a year end of December 31. Prepare all of the entries required for the note in 2020 and 2021.arrow_forward

- The Ombudsman Foundation is a private not-for-profit organization providing training in dispute resolution and conflict management. The Foundation had the following preclosing trial balance at December 31, 2020, the end of its fiscal year: Trial Balance—December 31, 2020 Debits Credits Accounts payable $ 25,400 Accounts receivable (net) $ 47,200 Accrued interest receivable 16,700 Accumulated depreciation 3,512,200 Cash 118,400 Contributed services 26,500 Contributions—no restrictions 2,446,000 Contributions—purpose restrictions 796,000 Contributions—endowment 2,057,500 Current pledges receivable 81,800 Education program expenses 1,537,100 Fund-raising expenses 126,100 Investment revenue—purpose restrictions 93,700 Training seminars expenses 4,548,100 Land, buildings, and equipment 5,612,700…arrow_forward1. Maggio Company manufactures kitchen equipment used in hospitals. They distribute their products directly to the customer and, for the year ending 2019, they reported these revenues and expenses. Sales Revenue $985,000 Cost of Goods Sold $489,000 Operating Expenses $245,000 Use this information to construct an income statement for the year 2019. Operating Income Cash Retained Earnings Gross Profit Cost of Goods Sold Service Revenue Cost of Services Operating Expenses Sales Revenue PLEASE NOTE: You must enter the account names exactly as written above and all whole dollar amounts will be with "$" and commas as needed (i.e. $12,345). Maggio Company Income Statement for Year Ended 2019arrow_forwardRefer to RE6-8. On April 23, 2020, McKinncy Co. receives a check, from Mangold Corporation for 8,500. Prepare the journal entry for McKinncy to record the collection of the account previously written off.arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning