Concept explainers

(a)

Concept Introduction: The value analysis is more of a systematic production review which includes the purchase process and the design of product to make sure the costs are reduced. This can be done using a set of activities including the product designs to make use of parts that have low-tolerance which are affordable, to switch to the components that cost low, including standardization of the parts to ensure the volume discounts are achieved.

To Prepare: The value analysis schedule and the determination and distribution of excess schedules.

(a)

Explanation of Solution

Given: Quail company purchases 80 of the common stock of Commo Company for $800000. At the time of purchase, Commo has framed its balance sheet.

Calculating fair value of total assets.

Fair value of total assets = Cash equivalents + Inventory + Land + Building + Equipment

Calculating net liabilities,

Net liabilities = Current liabilities + Bonds payable

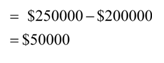

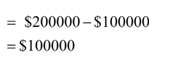

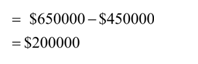

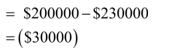

Now, calculate the fair value of net assets:

Fair value of net assets = Fair value of total assets - Liabilities payable = $1420000-$600000 = $820000

Value analysis schedule.

| Value analysis Schedule | Company-implied fair value | Parent Price (80%) | Non-controlling interest value (20%) |

| Company fair value | $1000000 | $800000 | $200000 |

| Fair value of net assets excluding | $820000 | $656000 | $164000 |

| Goodwill | $180000 | $1440000 | $36000 |

Along with total equity and excess of fair value over book value.

| Value analysis Schedule | Company-implied fair value | Parent Price (80%) | Non-controlling interest value (20%) |

| Fair value of subsidiary | $1000000 | $800000 | $200000 |

| Less: Book value of interest acquired Common stock Paid-in capital excess of par | $100000 $150000 $250000 | ||

| Total equity | $500000 | $500000 | $500000 |

| Interest acquired | 80% | 20% | |

| Book value (b) | $500000 | $400000 | $100000 |

| Excess of fair value over book value (a)-(b) | $500000 | $400000 | $100000 |

Inventory Adjustment = Fair value - book value

Land Adjustment = Fair value - book value

Building Adjustment = Fair value - book value

Equipment Adjustment = Fair value - book value

Adjustment of Identifiable Accounts

| Particulars | Adjustments | Worksheet key |

| Inventory | $1000000 | Debit D1 |

| Land | $100000 | Debit D2 |

| Building | $200000 | Debit D3 |

| Equipment | (30000) | Credit D4 |

| Goodwill | $180000 | Debit D5 |

| Total | $500000 |

(b)

Concept Introduction: The value analysis is more of a systematic production review which includes the purchase process and the design of product to make sure the costs are reduced. This can be done using a set of activities including the product designs to make use of parts that have low-tolerance which are affordable, to switch to the components that cost low, including standardization of the parts to ensure the volume discounts are achieved.

The value analysis schedule and the determination and distribution of excess schedules.

(b)

Explanation of Solution

Given: Quail company purchases 80% of the common stock of Commo Company for $800000. At the time of purchase, Commo has framed its balance sheet.

Market value of shares = Total number of shares x value per share

= 4000 shares x $45 per share = $980000

Goodwill under market value

| Value analysis Schedule | Company-implied fair value | Parent Price (80%) | Non-controlling interest value (20%) |

| Fair value of company | $980000 | $800000 | $180000 |

| Fair value of net assets excluding goodwill | $820000 | $656000 | $164000 |

| Goodwill | $160000 | $144000 | $16000 |

Value analysis schedule

| Value analysis Schedule | Company-implied fair value | Parent Price (80%) | Non-controlling interest value (20%) |

| Fair value of subsidiary (a) | $980000 | $800000 | $180000 |

| Less: Book value of interest acquired Common stock Paid-in capital excess of par retained earnings | $100000 $150000 $250000 | ||

| Total equity | $500000 | $500000 | $500000 |

| Interest acquired | 80% | 20% | |

| Book value (b) | $500000 | $400000 | $100000 |

| Excess of fair value over book value (a)-(b) | $500000 | $400000 | $100000 |

Adjustment of identifiable accounts

| Particulars | Adjustments | Worksheet Key |

| Inventory | $50000 | Debit D1 |

| Land | $100000 | Debit D2 |

| Building | $200000 | Debit D3 |

| equipment | ($30000) | Credit D4 |

| Goodwill | $160000 | Debit D6 |

| Total | $480000 |

c.

Concept Introduction: The value analysis is more of a systematic production review which includes the purchase process and the design of product to make sure the costs are reduced. This can be done using a set of activities including the product designs to make use of parts that have low-tolerance which are affordable, to switch to the components that cost low, including standardization of the parts to ensure the volume discounts are achieved.

The value analysis schedule and the determination and distribution of excess schedules.

c.

Explanation of Solution

Given: Quail company purchases 80 of the common stock of Commo Company for $800000. At the time of purchase, Commo has framed its balance sheet.

Value analysis schedule

| Value analysis Schedule | Company-implied fair value | Parent Price (80%) | Non-controlling interest value (20%) |

| Fair value of subsidiary (a) | $964000 | $800000 | $164000 |

| Less: Book value of interest acquired Common stock Paid-in capital excess of par retained earnings | $100000 $150000 $250000 | ||

| Total equity | $500000 | $500000 | $500000 |

| Interest acquired | 80% | 20% | |

| Book value (b) | $500000 | $400000 | $100000 |

| Excess of fair value over book value (a)-(b) | $464000 | $400000 | $64000 |

Adjustment of Identifiable Accounts

| Particulars | Adjustments | Worksheet Key |

| Inventory | $50000 | Debit D1 |

| Land | $100000 | Debit D2 |

| Building | $200000 | Debit D3 |

| equipment | ($30000) | Credit D4 |

| Goodwill | $144000 | Debit D6 |

| Total | $464000 |

Want to see more full solutions like this?

Chapter 2 Solutions

Advanced Accounting

- A fixed asset with a cost of $25,974 and accumulated depreciation of $23,377 is traded for a similar asset priced at $40,828 (fair market value) in a transaction with commercial substance. Assuming a trade-in allowance of $4,683, the cost basis of the new asset is Select the correct answer. $43,425 $38,742 $40,828 $36,145arrow_forward5. How should accounting fees for acquisition be treated? A. Expensed in the period of acquisition B. Capitalized as part of acquisition cost C. Deferred and amortized D. Deferred until the company is disposed of or wound-up 6.The excess of the price paid over the fair value of the net identifiable assets acquired should be recognized as A. Goodwill to be amortized periodically for 20 yearS. B. Expenses immediately C. Goodwill not subject to amortization but subject to impairment D. Goodwill to be amortized for 40 years 7.Under PFRS 3 (Business Combinations) A. Both direct and indirect costs are to be capitalized B. Both direct and indirect costs are to be expensed C. Direct costs are to be capitalized and indirect costs are to be expensed D. Indirect costs are to be capitalized and direct costs are to be expensedarrow_forwardProblem 15-5 (IAA) Prepare journal entry to record the sale`of ABC ordinary statement of financial position on January 1, 2020: Aborigine Company reported the following accounts in the share on July 1, 2021. Market adjustment for unrealized loss the change in fair value. 3. Prepare journal entry on December 31, 2021 to recognize A tement of hnancial position on January 1, 2020: Noncurrent assets Financial asset –FVOCI Market adjustment for unrealized loss 4,000,000 ( 500,000) Market value 3,500,000 Other comprehensive income Unrealized loss ( 500,000) An analysis of the investment portfolio revealed the following on December 31, 2020. Cost Market XYZ ordinary share ABC ordinary share RST preference share 1,000,000 2,500,000 500,000 1,200,000 2,000,000 200,000 4,000,000 3,400,000 On July 1, 2021, the ABC ordinary share was sold for P2,100,000. On December 31, 2021, the remaining investments have the following market value: XYZ ordinary share RST preference share 1,000,000 150,000…arrow_forward

- (1) Goodwill Calculation: Goodwill is the excess of the purchase consideration transferred over the fair value of the identifiable net assets acquired. Goodwill = Purchase Consideration - Fair Value of Identifiable Net Assets Purchase Consideration = Fair value of Black's investment + Fair value of non- controlling interest Purchase Consideration (21,000,000 + 21,000) + 11,800,000 Identifiable Net Assets = (40,000 + 3,890 +6,280 +2,570) (2,480 + 10,000) Goodwill (21,021,000) + 11,800,000-(52,740) Goodwill = 32,768, 260-52,740 Goodwill = 32,715, 520 Explanation: Goodwill arising on the acquisition of white is RM 32, 715,520 Can you do it in a debit credit format?arrow_forwardProblem 6. Sales and Leaseback On Januar y 1 20х1, Entity sold building to Entity and a simultaneously leased it back. Additional information follows : Fair value of building 1,000,000 Carrying amount of building 800,000 Remaining useful life of building 10 years Lease Term 5 years Annual rent payable at the end of each year 100,000 Implicit interest rate equal to market rate 12% The transfer qualifies as a sale. Requirements (Independent cases) : а. If the sales price is P1,000,000 which is equal to fair value compute t he following under the seller-lessee accounting i. Lease liability ii. Right of use Asset iii. Gain or Loss iv. Journal entries on January 1, 20x1 b. If the sales price is P1,000,000 which is equal to fair value compute the following under the buyer-lessor acco unting i. Gross Investment ii. Net Investment iii. Unearned Interest Income iv. Journal entries on January 1, 20x1 c. Same requirements in a and b but the sales price is P1,100,000 which is above the fair value…arrow_forwardThe following pertains to Connie Corp's biological assets: Fair value based on unobservable inputs for the asset P4,900 Quoted price in an active market for similar asset P5,400 Quoted price in an active market for identical asset P5,300 Selling price in a binding contract to sell P5,600 Estimated commissions to brokers and dealers P500 Estimated transport and other costs necessary to get asset to the market P300 The entity’s biological assets should be valued atarrow_forward

- A fixed asset with a cost of $24,737 and accumulated depreciation of $22,263 is traded for a similar asset priced at $60,057 (fair market value) in a transaction with a commercial substance. Assuming a trade-in allowance of $4,264, at what cost will the new equipment be recorded in the books? a.$4,264 b.$1,790 c.$60,057 d.$20,473arrow_forwardIf the company's assets in TL: cash 100.000, accounts receivable 50.000, inventory 150.000, and building 200.000 (market value 300.000) and the liabilities 300.000. If the price paid to acquire company 400.000 TL, how much is the goodwill under market value approach? Select one: a. 100.000 b. 300.000 c. 200.000 d. 150.000arrow_forwardA fixed asset with a cost of $21,296 and accumulated depreciation of $19,166 is traded for a similar asset priced at $68,841 (fair market value) in a transaction with commercial substance. Assuming a trade-in allowance of $4,779, at what cost will the new equipment be recorded in the books? a.$68,841 b.$64,062 c.$66,192 d.$70,971A fixed asset with a cost of $21,296 and accumulated depreciation of $19,166 is traded for a similar asset priced at $68,841 (fair market value) in a transaction with commercial substance. Assuming a trade-in allowance of $4,779, at what cost will the new equipment be recorded in the books? a.$68,841 b.$64,062 c.$66,192 d.$70,971A fixed asset with a cost of $21,296 and accumulated depreciation of $19,166 is traded for a similar asset priced at $68,841 (fair market value) in a transaction with commercial substance. Assuming a trade-in allowance of $4,779, at what cost will the new equipment be recorded in the books? a.$68,841 b.$64,062 c.$66,192 d.$70,971A…arrow_forward

- E3.5 Acquisition analysis, including fair value adjustment for plant and equipment (Section 3.6.2) On 1 October 20XO, EF Ltd acquired all the issued ordinary shares of GH Ltd. The terms of the acquisition agreement specified that EF Ltd must pay the existing shareholders of GH Ltd $1.5million immediately and a further $1.5million on 30 September 20X1. The incremental cost of short-term finance to EF Ltd is 10% p.a. At acquisition date, the issued capital and reserves of GH Ltd were as follows: Issued capital 1 200000 Retained eamings 1/10/20X0 1400000 At 1 October 20xO, the plant and equipment of GH Ltd had a carrying amount that was $150000 less than its fair value. The company income tax rate is 30%. REQUIRED (a) Prepare the general journal entries for the accounting records of EF Ltd to record: (i) the investment in GH Ltd on 1 October 20X0 (ii) the cash payment of the $1500 000 on 30 September 20X1.arrow_forwardA fixed asset with a cost of $28,202 and accumulated depreciation of $25,382 is traded for a similar asset priced at $55,381. Assuming a trade-in allowance of $4,724, the cost basis of the new asset in a transaction with commercial substance is Select the correct answer. $55,381 $23,478 $1,904 $4,724arrow_forward16. ABC Co.'s biological asset has a fair value less costs to sell of P 100,000 and P120,000, respectively. The year-end adjusting entry will most likely include a. a credit to unrealized gain of P 20,000 to be recognized in profit or loss b. a credit to unrealized gain of P 20, 000 to be recognized in other comprehensive income c. a debit to unrealized gain of P 20,000 to be recognized in profit or loss d. none of thesearrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT