Videos

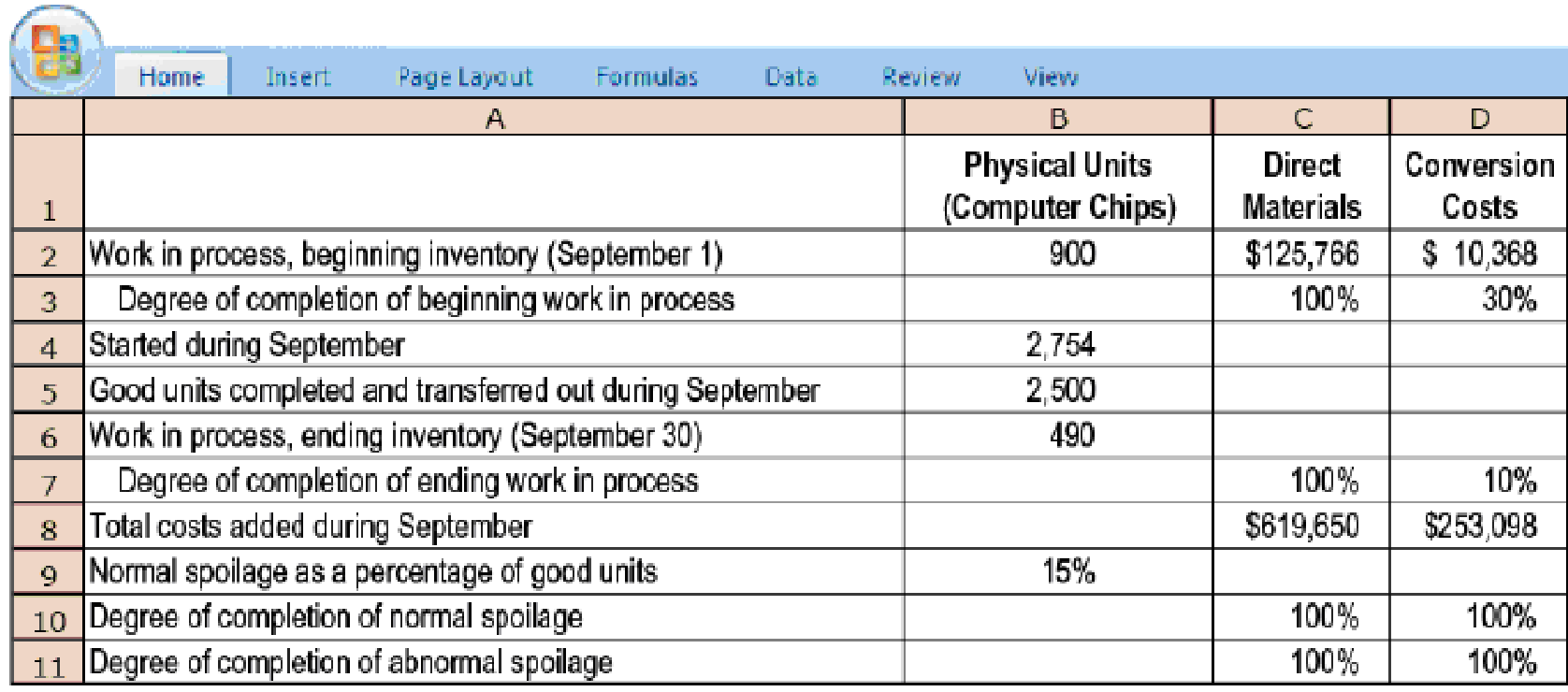

Weighted-average method, spoilage. LogicCo is a fast-growing manufacturer of computer chips. Direct materials are added at the start of the production process. Conversion costs are added evenly during the process. Some units of this product are spoiled as a result of defects not detectable before inspection of finished goods. Spoiled units are disposed of at zero net disposal value. LogicCo uses the weighted-average method of

Summary data for September 2017 are as follows:

- 1. For each cost category, compute equivalent units. Show physical units in the first column of your schedule.

Required

- 2. Summarize the total costs to account for; calculate the cost per equivalent unit for each cost category; and assign costs to units completed and transferred out (including normal spoilage), to abnormal spoilage, and to units in ending work in process.

Want to see the full answer?

Check out a sample textbook solution

Chapter 18 Solutions

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Additional Business Textbook Solutions

Principles of Accounting Volume 2

Managerial Accounting (4th Edition)

Managerial Accounting: Tools for Business Decision Making

FINANCIAL ACCT.FUND.(LOOSELEAF)

Financial Accounting, Student Value Edition (5th Edition)

Principles Of Taxation For Business And Investment Planning 2020 Edition

- LogicCO is a fast-growing manufacturer of computer chips. Direct materials are added at the start of the production process. Conversion costs are added evenly during the process. Some units of this product are spoiled as a result of defects not detectable before inspection of finished goods. Spoiled units are disposed of at zero net disposal value. uses the FIFO method of process costing. Summary data and weighted-average data for are as follows: Requirements : 1. For each cost category, compute equivalent units. Show physical units in the first column. 2. Summarize total costs to account for; calculate cost per equivalent unit for each cost category; and assign costs to units completed and transferred out (including normal spoilage), to abnormal spoilage, and to units in ending work in process. 3. Should 's managers choose the weighted-average method or the FIFO method? Explain.arrow_forwardWeighted-average method, spoilage, equivalent units. (CMA, adapted) Consider the following data for November 2017 from MacLean Manufacturing Company, which makes silk pennants and uses a process-costing system. All direct materials are added at the beginning of the process, and conversion costs are added evenly during the process. Spoilage is detected upon inspection at the completion of the process. Spoiled units are disposed of at zero net disposal value. MacLean Manufacturing Company uses the weighted-average method of process costing.arrow_forwardArklan Production is upgrading its manufacturing process from a manual process to a highly automated system. Management believes that the new system will result in greater efficiencies and a better finished product. Arklan is also working on a plan to downsize staff after the implementation of the new system. Arklan has used a traditional absorption costing system to calculate unit product costs for external financial reporting. In the past, Arklan has allocated its manufacturing overhead costs using a predetermined plant-wide overhead rate based on direct labor hours. The controller realizes that the new system may require changing the overhead allocation process. Management plans to take the opportunity to reconsider other improvements to the costing system. Identify and explain three benefits of using departmental overhead rates to allocate overhead costs. Explain the difference between absorption costing and variable costing. Identify which is more suitable for internal…arrow_forward

- Rounder specializes in the manufacture of ball bearings for aircraft. Direct materials are added at the start of the production process. Conversion costs are added evenly during the process. Some units of this product are spoiled as a result of defects not detectable before inspection of finished goods. Normally, the spoiled units are 15% of the good units transferred out. Spoiled units are disposed of at zero net disposal price. Suppose Rounder determines standard costs of $246 per (equivalent) unit for direct materials and $96 per (equivalent) unit for conversion costs for both beginning work in process and work done in the current period. Summary data for September are: (Click the icon to view the data.) Required 1. For each cost element, compute the equivalent units. Show physical units in the first column. 2. For each cost element, calculate the cost per equivalent unit. 3. Summarize the total costs to account for, and assign these costs to units completed and transferred out (to…arrow_forward4. Considering the following data for April 2018 from Pink Manufacturing Company, which makes silk pennants and uses FIFO Process Costing. All direct materials are added at the beginning of the costing process, and conversion costs are added evenly during the process. Spoilage is detected upon inspection at the completion of the process. Spoiled units are disposed at a zero net disposal value. Physical Direct Units Direct Materials Conversion Costs Work in process, April 1 Started in April Completed and transferred out 1,000 P14,230 P11,100 ? 9,000 Normal lost units 100 Abnormal lost units 50 Work in process, April 30 Costs added during April 2,000 P121,180 P277,500 Stages of Completion of Work in Process Materials Conversion Costs Beginning 100% 50% Ending 100% 30% Requirement: 1.What are the equivalent units for materials and conversion cost? 2. What is cost per equivalent units for materials and conversion costs (rounded)? 2.What is the cost of the units completed and transferred…arrow_forwardPlease show your computations using good accounting form through excel. Thank you! Problem: By products In Department III of SAMCIS Company, a portion of the materials (a by-product) is removed further processed and sold. The Company uses the reversal cost method to account for the by-product. Data for June include: Amount of by-product removed is 2,000 units; Estimated sales price of by-product after processing further is P1.20/unit. Estimated processing cost after separation is P0.30 per unit and estimated selling expenses is 10% of the sales price. The estimated profit margin is 5% of the sales price. What is the gain (loss) on sale of the by-product if all of the units are sold at P1.50?arrow_forward

- Aboksh Ltd. operates a System of Standard Costing. The company manufactures a Chemical Product by mixing three ingredients Chemicals A, B and C and processes the same. The Standard Cost data for the product are as follows : Chemical Percentage of Total Input Standard Cost per kg. ($) А 50% 40 30% 60 20% 95 Note : Loss during processing is 5% of input and this has no realizable value. During the month of May, 2018, 10,200 kg. of finished product was obtained from the inputs as per details given below : Quantity purchased and issued Chemical Consитed Actual Cost ( $) 5,200 kg. 3,600 kg. 1700 kg. А 2,34,000 В 2,19,600 C 1,58,100 You are required to calculate : (i) Material Cost Variance, (ii) Material Price Variance.arrow_forwardPlease show your computations using good accounting form through excel. Thank you! Problem: By products In Department III of SAMCIS Company, a portion of the materials (a by-product) is removed further processed and sold. The Company uses the reversal cost method to account for the by-product. Data for June include: Amount of by-product removed is 2000 units; Estimated sales price of by-product after processing further is P1.20/unit. Estimated processing cost after separation is P0.30 per unit and estimated selling expenses is 10% of the sales price. The estimated profit margin is 5% of the sales price. What is the total cost of the by-product?arrow_forwardTechno Instruments uses a manufacturing costing system with one direct-cost category (direct materials) and three indirect-cost categories: a. Setup, production-order, and materials-handling costs that vary with the number of batches b. Manufacturing-operations costs that vary with machine-hours c. Costs of engineering changes that vary with the number of engineering changes made In response to competitive pressures at the end of 2016, Techno Instruments used value-engineering techniques to reduce manufacturing costs. Actual information for 2016 and 2017 is as follows: 2016 2017 Setup, production-order, and materials-handling costs per batch $8,600 $7,800 Total manufacturing-operations cost per machine-hour $59 $53 Cost per engineering change $18,750 $14,000 The management of Techno Instruments wants to evaluate whether value engineering has succeeded in reducing the target manufacturing cost per unit of one…arrow_forward

- Grace Company manufactures picture frames of all sizes and shapes and uses job-order costing system. There is always some spoilage in each production run. The following costs relate to the current run: Estimated overhead (exclusive of spoilage) Spoilage (estimated) Sales value of spoiled frames Labor hours P 160,000 25,000 11,500 100,000 The actual cost of a spoiled picture frame is P7.00. During the year, 170 frames are considered spoiled. Each spoiled frame can be sold for P4. The spoilage is considered a part of all jobs (factory overhead). What amount should be debited to Factory Overhead Control to record spoilage pertaining to unrecovered cost?arrow_forwardZett Company has been using FIFO process costing for tracking the costs of its manufacturing activities. But, in recent months, the system has become somewhat bogged down with details. It seems that, when the company purchased ABB Electronics last year, its product lines increased six-fold. This has caused both the accountants and the suppliers of the information, the line managers, great difficulty in keeping the costs of each product line separate. Likewise, the estimation of the completion of ending work-in-process inventories and the associated costs has become very cumbersome. The CFO of the company is looking for ways to improve the reporting system of product costs. What can you recommend to improve the situation?arrow_forwardThe management of Gregory Corporation believes that the inspection cost is a mixed cost that depends on units produced. The high- low method is used to estimate the variable and fixed components of this cost. The total inspection costs at Gregory's factory are listed below. Month Units Produced Inspection Cost January 990 S21,730 February 985 $21,645 March 807 SIR619 April 650 SI5,950 May 760 $17,820 June 870 S19,690 July 805 SI8,585 August 810 SIRA0 September 700 S16,300 5. What is the variable cost per unit? * $8.50 per unit $17.00 per unit $21.95 per unit $22.98 per unit None of the abovearrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning