Videos

Accounting concepts

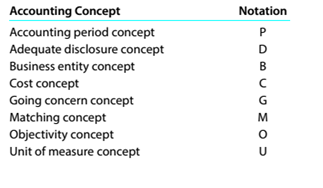

Match each of the following statements with the appropriate accounting concept. Sonic concepts may he used more than once, while others may not be used at all. Use the notat ions shown to indicate the appropriate accounting concept.

Statements

1. Assume that a business will continue forever.

2. Material litigation involving the corporation is described in a note.

3. Monthly utilities costs are reported as expenses along with the monthly revenues.

4. Personal transactions of owners are kept separate from the business.

5. This concept supports relying on an independent actuary (statistician), rather than the chief operating officer of the coq)ration, to estimate a pension liability.

6. Changes in the use of accounting methods from one period to the next are described in the notes to the financial statements.

7. Land worth $800,000 is reported at its original purchase price of $220,000.

8. This concept justifies recording only transactions that are expressed in dollars.

9. If this concept was ignored, the confidence of users in the financial statements could not be maintained.

10. The changes in financial condition are reported at the end of the month.

Trending nowThis is a popular solution!

Chapter 1 Solutions

Survey of Accounting (Accounting I)

Additional Business Textbook Solutions

Horngren's Accounting (11th Edition)

Advanced Financial Accounting

Principles Of Taxation For Business And Investment Planning 2020 Edition

Managerial Accounting: Tools for Business Decision Making

Managerial Accounting (5th Edition)

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

- True or False for the following statements: 1. Accounting can be defined as an information system that provides reports to users about the economic activities and condition of a business. 2. An account receivable is typically classified as a revenue, not an asset. 3. The allowance for doubtful accounts is an estimate based on past experience of the corporation. 4. Using FIFO method to calculate inventory can decrease tax payment. 5. The accounting equation can be expressed as Assets - Liabilities = Owner's Equity 6. If the liabilities owed by a business total S300,000 and owners equity is equal to $300,000, then the assets also total $300,000. 7. An account receivable is a claim against a customer arising from a sale on account. 8. The unit of measure concept requires that economic data be recorded in a common unit of measurement like RMB and U.S. dollar. 9. Paying off an account payable increases liabilities. 10. The normal balance of cash account is a debit.arrow_forwardAccounting provides information on Select one: O a. All of the answers are correct O b. Financial conditions of an institution O c. Company's tax liability for a particular year O d. Cost and income for managersarrow_forwardAccounting principles that assumes the entity will continue to operate indefinitely and financial statements are prepared on the basis that the business will continue for the foreseeable future are: Select one: A. going concern B. separate entity C. accrual basis D. historical concepts What is the meaning of accounts? Select one: A. The details of business transactions are supported by source documents B. are withdrawals and expenses that are deducted from owner’s equity C. An error that was made in carrying the account balance to the trial balance D. the basic storage units for accounting data Bookkeeping: Select one: A. consist of the interconnected business subsystems. B. a business unit chartered by the state and legally separate from its owners C. including accounting, that provide the information needed to run a business. D. is the process of recording financial transactions and keeping financial records. It is mechanical and repetitive and is usually…arrow_forward

- . A list of concepts is provided below in the left column, with descriptions of the concepts in the right column. There are more descriptions provided than concepts. Match the description to the concept. ________ Cash-basis accounting. ______ Fiscal year. _______ Revenue recognition principle. _______ Expense recognition principle. (a) Monthly and quarterly time periods. (b) Accountants divide the economic life of a business into artificial time periods. (c) Efforts (expenses) should be recognized in the period in which a company consumes assets or incurs liabilities to generate accomplishments (revenues). (d) An accounting time period that starts on January 1 and ends on December 31. (e) An accounting time period that is one year in length. (f) Companies record revenues when they receive cash and record expenses when they pay out cash. (g) Companies record transactions in the period in which the events occur. (h) Recognize revenue in the accounting period in which a performance…arrow_forward1.Assets = Liabilities + (Owner, Capital - Owner, Withdrawal + Revenues - Expenses)2. What is a company's financial obligation that results in the company’s future sacrifices of economic benefits to other entities or businesses?3. What is considered as the residual claims on assets?4. What do you call the chronological record of all the financial transactions of a business which is also known as the book of original entry?5. TRUE or FALSE? Debit means increases while credit means decreases.6. What accounting principle dictates that companies recognize revenue as it is earned, and not when they receive payment?7. Which of the four accounts is NOT a liability? Unearned revenue; Accrued expense; Accounts payable; Accounts receivable8. The following accounts must be closed at the of the accounting period, EXCEPT: Equity, revenue, expense, income summary9. What inventory system continuously estimates the inventory based on the running electronic…arrow_forwardFill in the blanks for the missing elements in the following three statements: Corporation _____________ transactions are tracked in two different accounts; ________________accounts track owner contributions separately from earnings. Earnings and earning distributions are tracked in the __________________________ account.arrow_forward

- Give typing answer with explanation and conclusion 1. ________ are items owed to a creditor. ________ are items owned by a company. ________ represents owners' claims to company resources. Expenses; Revenues; Net income Expenses; Revenues; Stockholders��� equity Liabilities; Assets; Stockholders' equity Liabilities; Assets; Net incomearrow_forwarda. What do the accounting policies say in the annual report (footnotes) regarding the cost of revenue? What are the drivers to the cost of revenue and the trends? b. Are there any trends in sales and marketing expenses or research and development? Are these amounts reasonable for the type of business? c. Compare general and administrative expenses to similar companies. Are they reasonable? d. What is the ratio of net interest income (expense) to income from operations? Is this a safe ratio for the company? Why or why not?arrow_forwardACCOUNTING MULTIPLE CHOICE QUESTIONS. ANSWER ALL IF POSSIBLE An account balance is: A. The total of the credit side of the account B. The total of the debit side of the account C. The difference between the total debits and total credits for an account including the beginning balance D. Always a credit Show Transcribed Text O Businesses can take any of the following forms of business ownership except: A. Sole proprietorship C. Joint Offering B. Partnership D. Corporation FOB shipping point means that the A. goods are placed free on board to the buyer's place of business. B. buyer pays the freight. Show Transcribed Text 3 C. seller pays the freight. D. common carrier pays the freight. C Show Transcribed Text Income from operations is A. Net sales less Cost of goods sold. B. Net sales less Operating expenses. C. Gross profit less Other expenses and losses. D. Gross profit less Operating expenses. When completing a bank reconciliation, what action should you take regarding "Outstanding…arrow_forward

- Answer the following question1) Explain the purpose of GAAP (Generally Accepted Accounting Principles), including the organization currently responsible for the creation and governance of these standards?2) How are assets and liabilities classified as either current or long term? Explain with example. 3) If a business had a net loss for the year, what would be the closing entry to close income summary and transfer the net loss to the capital account? Explain with example.4) The statement of changes in financial position was designed to enable financial statement users to answer questions like these:a) Where did the profit go?b) What do you mean by dividend? Explainc) How was it possible to distribute dividends in the presence of a loss?arrow_forward1-Accounting software is related to which system of accounting? a. Manual Individual customer records b. Manual system of accounting c. Computerized accounting d. Any system of accounting 2-A Creditor of the business uses the financial statement for a. Day to day decision making related to the business b. Making the decisions to buy or sell the shares c. Evaluating the risks of granting credit or lending money d. Verifying whether the company complies with tax laws 3-For every debit there will be an equal credit according to a. Dual aspect concept b. Matching concept c. Money measurement concept d. Cost concept 4-Mr. Asif is an accountant. Purchase of Merchandise on credit for OMR 75000 was entered in Furniture Account for OMR 75000 but he posted Accounts payable entry is correct. Which of the following rectification entry is correct? a. Debit Accounts payable RO 75000 Credit Furniture RO 75000 b. Debit Purchase RO 75000 Credit Accounts payable account RO…arrow_forwardA. Identify the nature of each account using the letter A for assets, L for liabilities, SE for shareholders’ equity, R for revenue, E for expenses, and NA for not applicable. B. Calculate net income for the period. C. How much has been earned by the company’s operations but not distributed to shareholders? D. What is the total investment by shareholders? E. How much do customers owe the company?arrow_forward

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College